Management Discussion And Analysis

Business Reports

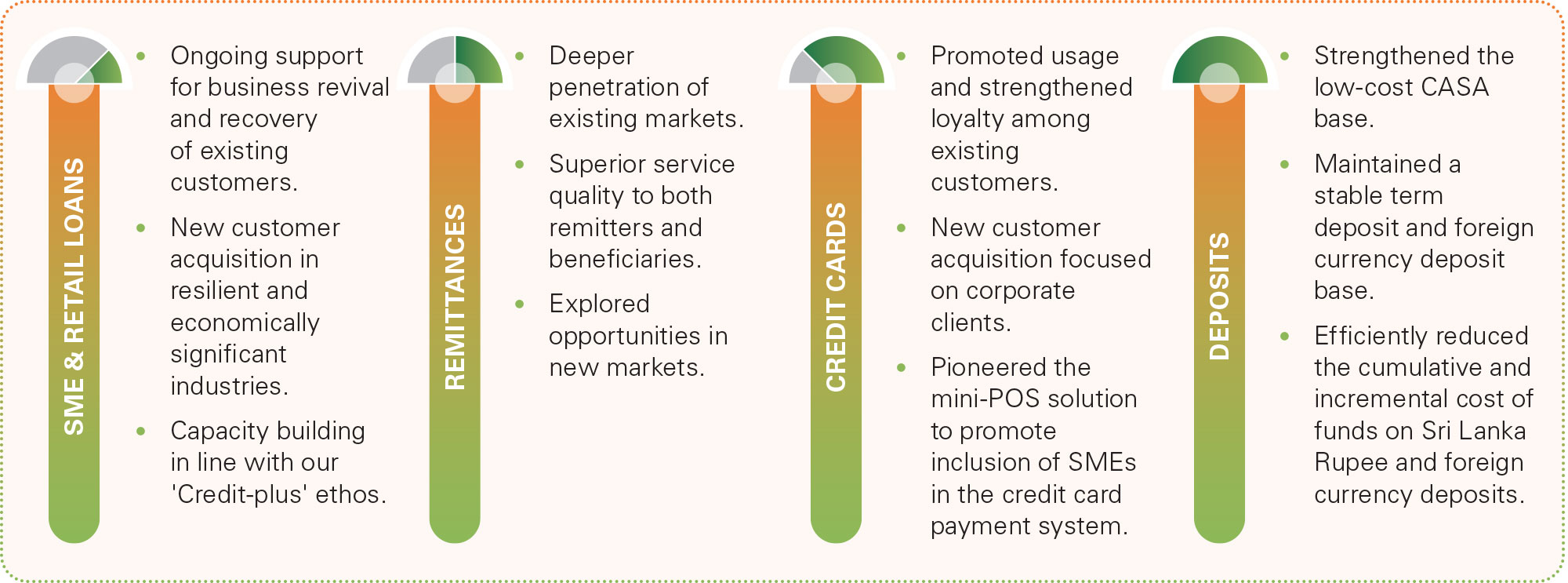

SME & Retail Banking which comprises the SME & Retail Lending, Credit Cards, Deposits and Remittance pillars focuses on supporting the financial needs of SME and retail customers. Together, these units provide customer-centric financial solutions that nurture the growth of the SME sector and fulfil the diverse financial needs of retail customers at different life stages. The Remittance Unit leverages its global presence to boost inward remittances, improving the financial well-being of families and supporting economic stability.

Rs 48.6 Bn

Segment Operating Profit 2024 (before tax)

Rs 1,545 Bn

Segment Assets 2024

Rs 1,506 Bn

Segment Liabilities 2024

Our Services

- Business Loans

- Refinance

- Factoring

- Trade Finance

- Housing Loans

- Personal Loans

- Pawning and Gold Loans

- Leasing

- E-Remittances

- Visa

- Mastercard

- Amex

- Affinity Cards

- Prepaid Cards

- Personal Debit Cards

- Corporate Credit Cards

- Merchant Services

- Current Accounts

- Savings Accounts

- Term Deposits

- Foreign Currency Accounts

Market Review

The stabilisation of the economy in 2024 facilitated the revival of business activity, positioning the SME sector on a trajectory of gradual recovery, underpinned by improving cashflows and repayment ability. The tourism, agriculture, trade, healthcare and manufacturing industries demonstrated growth, presenting opportunities for lending. However, the prevailing economic and political uncertainty tempered overall business sentiment, leading to a cautious approach towards expansion. The combined impact of elevated prices and tax adjustments continued to impact real income levels of retail customers, dampening consumer spending and appetite for retail credit.

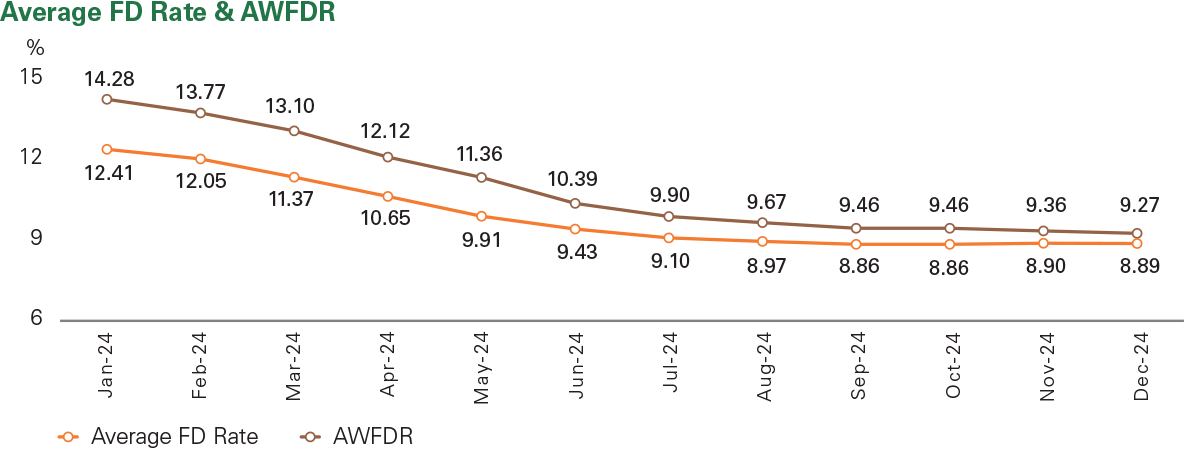

The cautious business climate presented opportunities for deposit growth, particularly in low-cost CASA deposits as businesses sought to maintain ready access to funding. This contributed to a lower cost of funding. However, the further decline in interest rates by 228 bps in 2024, following the 449 bps decline in 2023, resulted in a decline in interest income that outweighed the reduction in funding costs, adversely impacting net interest income.

Meanwhile, inflow of workers’ remittances maintained its growth momentum in 2024. The highest volumes of workers’ remittances were received from the GCC region, South Korea and Italy.

Aligning with the Bank’s overall long-term strategy of strengthening its presence in the SME sector, SME and Retail area was remodelled at the beginning of 2024. A range of roles and responsibilities was reorganised into separate specialised units, leading to the creation of a team of 16 Regional Managers.

Strategy

SME & Retail Loans

The Branch Banking structure was remodelled to create a dedicated team of Regional and Relationship Managers focused on lending to small and medium-sized enterprises to further the Bank’s growth strategy in the SME sector.

Delivering Results in 2024

| Performance Highlights | |||

|---|---|---|---|

| 2024 Rs Mn |

2023 Rs Mn |

Change % |

|

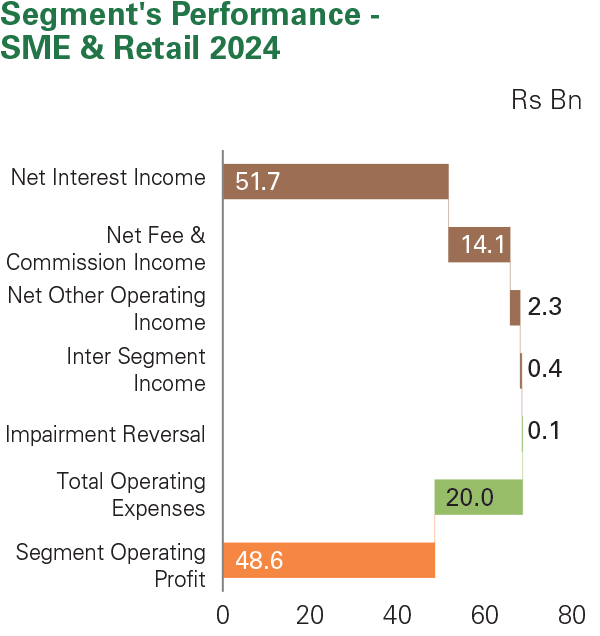

| Net interest income | 51,656 | 60,336 | (14.4) |

| Net fee & commission income | 14,137 | 14,375 | (1.7) |

| Net other operating income | 2,299 | 1,331 | 72.7 |

| Inter-segment income | 416 | 1,034 | (59.7) |

| Total operating income | 68,508 | 77,076 | (11.1) |

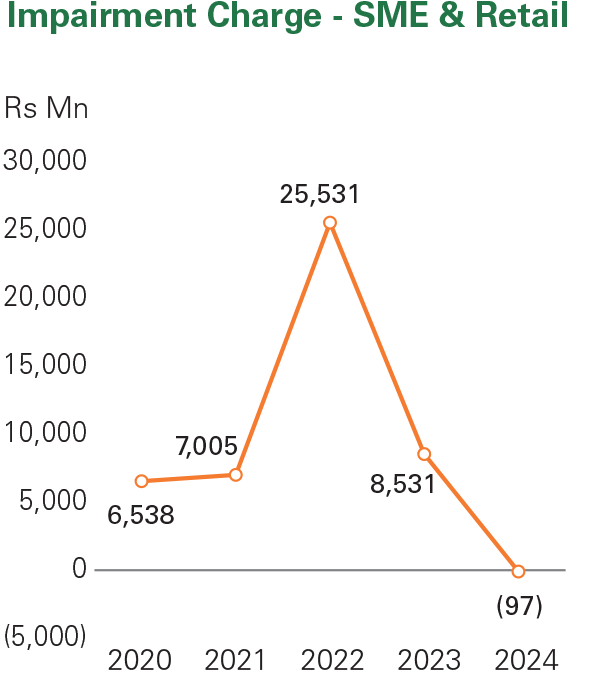

| Less: Impairment (reversal)/charge | (97) | 8,531 | (101.1) |

| Net operating income | 68,605 | 68,546 | 0.1 |

| Less: Total operating expenses | 19,989 | 17,366 | 15.1 |

| Operating profit before tax | 48,616 | 51,179 | (5.0) |

| Segment assets | 1,545,080 | 1,341,134 | 15.2 |

| Segment liabilities | 1,505,862 | 1,299,613 | 15.9 |

Note: The segment assets, liabilities, income, and expenses figures mentioned above include inter-segment balances.

EMPOWERING COMMUNITIES THROUGH FINANCIAL INCLUSION

Enabling access to finance for communities across the nation

-

An island-wide geographic presence promoting financial accessibility

across;

Branches

Branches229

ATMs

ATMs260

CRMs

CRMs295

CDMs

CDMs234

eZ Banking Agents

eZ Banking Agents1,252

Digital Banking Centres

Digital Banking Centres32

- Innovative digital solutions with trilingual capability enabling,

- 24/7 accessibility

- Island-wide reach

- Enhanced convenience to customers and businesses

- Support the specific needs of small businesses

Pioneered the introduction of the mini-POS enabling the inclusion of SMEs into the credit card payment system expanding their revenue opportunities.

A PRODUCT PORTFOLIO THAT CATERS TO THE NEEDS OF OUR COMMUNITIES

A ‘CREDIT PLUS’ ETHOS FOSTERING FINANCIAL KNOWLEDGE AND SKILLS WITHIN OUR COMMUNITIES

We strive to elevate businesses by providing comprehensive financial support which extends beyond the mere provision of financing to include strengthening of financial capabilities and knowledge.

Support extended includes,

- Formal programmes on cash flow management.

- Leveraging partnerships to fuel business growth.

- One-on-one engagement with Regional Managers and Relationship Managers to optimise financial solutions according to business needs.

Our Impact

KEY BUSINESS NEEDS SUPPORTED IN 2024

Cash flow management

Business revival and recovery

Business growth

Capital investment

Business survival

SME & RETAIL LENDING

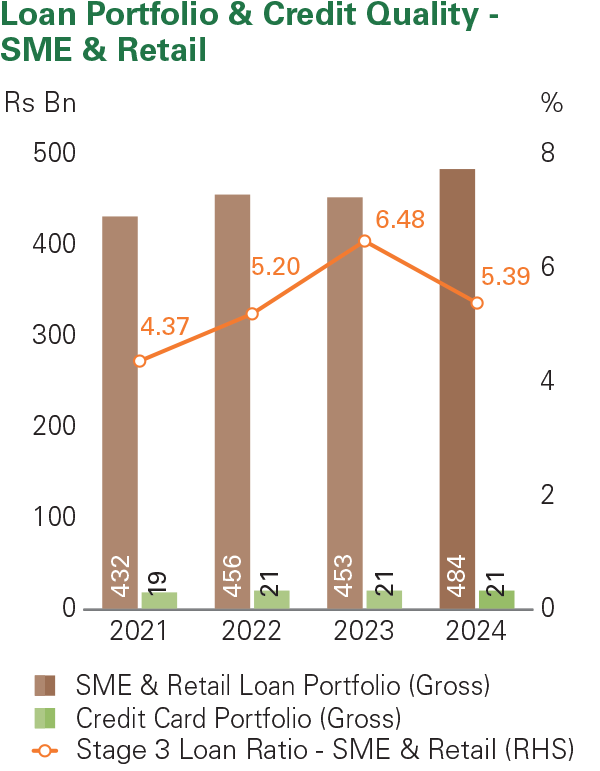

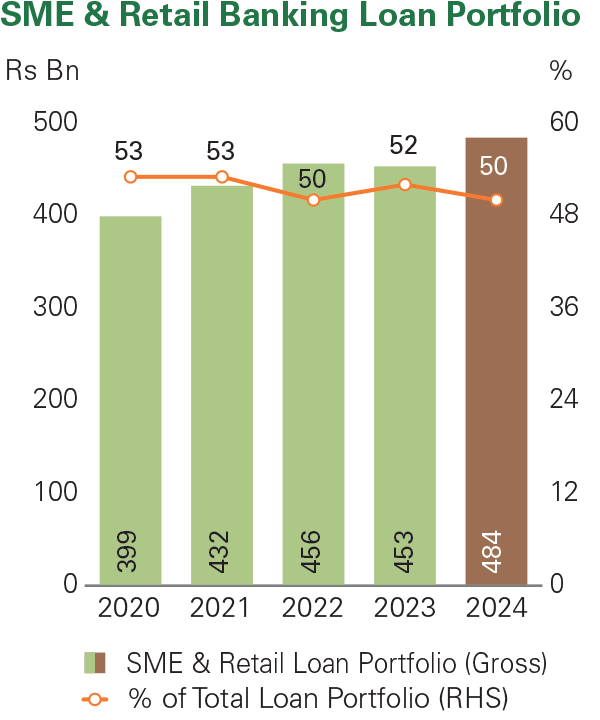

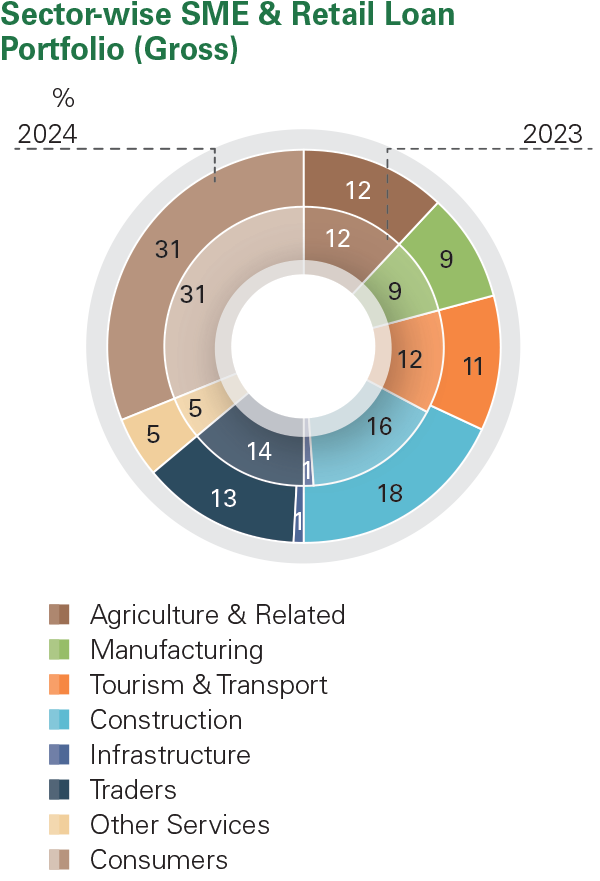

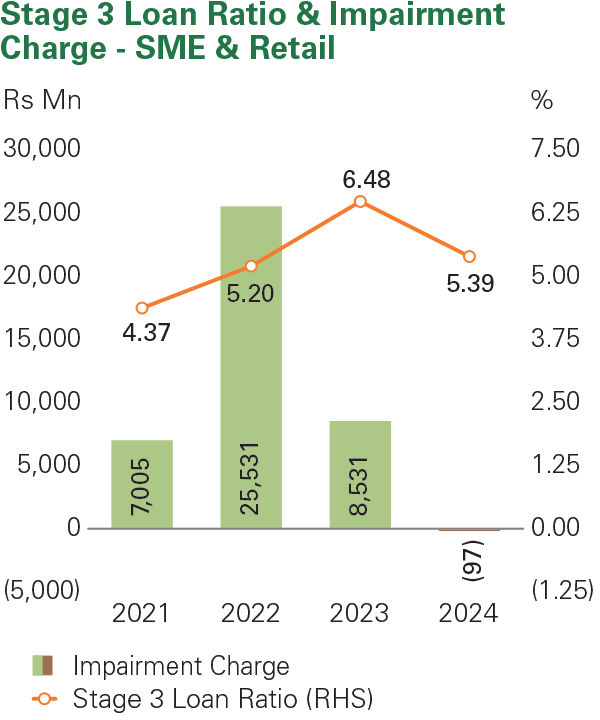

The branch network which caters to SME & retail customers, delivered stable performance in 2024, underpinned by a focused strategy that supported the revival and recovery of the SME sector and targeted growth in economically significant and resurging sectors. Accordingly, the SME & Retail loan portfolio expanded by 6.7% as at end-December 2024 and stemmed primarily from the tourism, healthcare, manufacturing, agriculture and trading industries. Robust, collaborative efforts at all levels, the expertise of the Recoveries Unit, ongoing customer engagement and customised restructuring solutions that matched the cash flows of recovering SMEs, facilitated improvements in stage II and stage III loan classifications as well as a reversal in impairment charges in 2024. Improving loan quality and declining funding costs supported an uptrend in the overall profitability during the year under review.

Aligning with the Bank’s overall long-term strategy of strengthening its presence in the SME sector, SME and Retail area was remodelled at the beginning of 2024. A range of roles and responsibilities was reorganised into separate specialised units, leading to the creation of a team of 16 Regional Managers located at Regional Offices, each with their respective teams, primarily focusing on capturing opportunities in the SME sector.

To enhance the new SME team’s capabilities, the newly appointed SME Relationship Managers participated in a 6-month training programme on SME financing. Accordingly, the newly designated SME Relationship Managers completed this programme in 2024.

The above remodelling process has led to streamlining of operations, enhanced service delivery and improved turnaround times for credit approvals.

Investments were also made to upgrade the IT infrastructure to streamline operations, support swifter service delivery and improve turnaround times for loan approvals. These efforts resulted in a notable reduction in customer complaints.

Given the integration of a significant number of new team members over the last two years, the Unit implemented a comprehensive training programme to ensure staff members possessed the skills required to fulfil their roles effectively and ensure high levels of service quality. Over 950 team members which accounted for over 35% of the Branch Banking team participated in the training programme conducted over the course of the year by senior staff members and included the development of technical and customer service competencies. These efforts have led to a notable reduction in customer complaints.

Recognising the extraordinary macroeconomic challenges faced by the SME sector in recent years, the scope of the Business Revival Unit (BRU) was expanded during the year under review in line with CBSL regulations to assist in reviving viable businesses impacted by these conditions. Businesses with potential for revival were assessed against specific eligibility criteria. Those meeting these criteria were transferred to the BRU, where a combination of financial and operational restructuring strategies were employed to revive distressed but viable businesses. In 2024, facilities extended to 66 businesses were transferred to the BRU to initiate their journey towards recovery.

Consistent with its ‘Credit plus’ ethos, the Unit committed to educating SME customers on financial statement preparation during the year under review. This included developing Excel based formats for financial statements and uploading them to the Sampath Vishwa SME – Persona platform for customers to download and familiarise themselves with. Regional Managers and SME – Relationship Managers actively engaged with SME customers to provide guidance and support in this regard. Additionally, the Bank also nominated suitable candidates for relevant capacity building programmes conducted by external institutions including the ADB. The Unit also utilised access to the ADB concessionary refinancing scheme to support SME sector development. Recognising the unique business needs of paddy millers and traders, the Unit introduced pledge loans and warehouse financing respectively during the year under review.

Fulfilling our social and environmental responsibilities by promoting sustainable business practices among customers remained a priority during the year under review. Concessionary rates were offered through the Sustainable Green Financing Scheme for projects that met specified environmental standards. The Unit also partnered with selected service providers to promote renewable energy solutions to customers.

SUSTAINABLE FINANCING SOLUTIONS

Green loans for projects that fulfil verified sustainability standards

Sustainable Green Financing Scheme

Partnerships to promote renewable energy solutions

Sampath Bank launched the first-ever Sampath Visa Infinite Metal Credit Card in Sri Lanka, joining an elite circle with access to privileges that span the globe, from exclusive rewards to unique travel benefits, making every transaction a seamless blend of convenience and prestige.

CREDIT CARDS

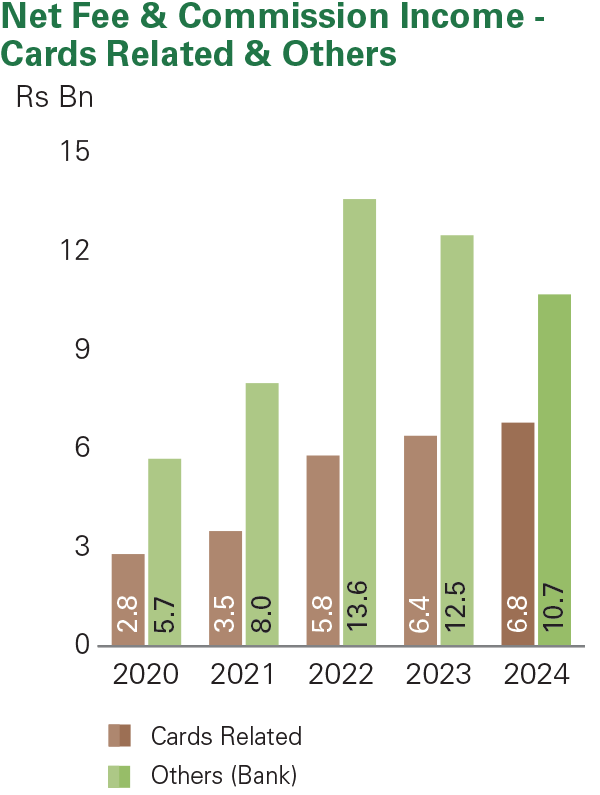

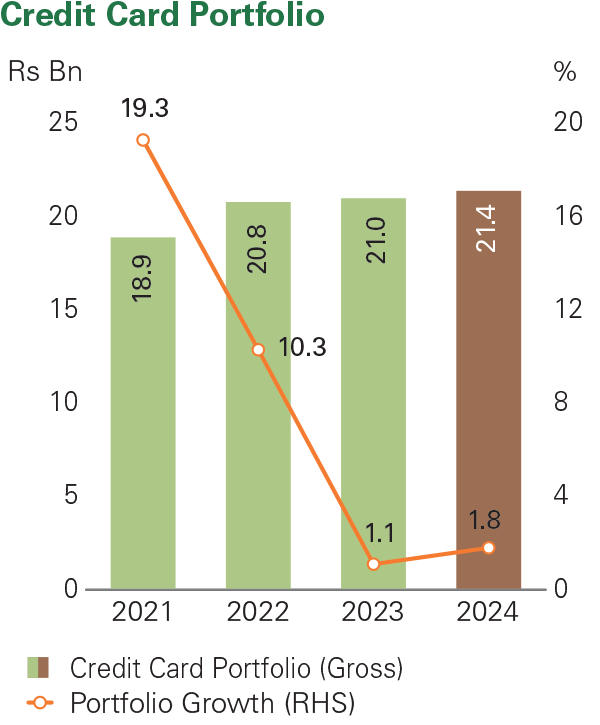

The Card Centre recorded stable performance in 2024, despite muted consumer spending and a cautious approach to new customer acquisition. Strategic emphasis was placed on strengthening loyalty and credit card spend of existing cardholders through unique and differentiated value propositions including lifestyle, experiential and entertainment promotions. To celebrate 35 years of providing credit card solutions, the Card Centre launched a brand building campaign which leveraged social media platforms and included exclusive promotional offers for cardholders. Cardholders were also offered 35-month extended settlement plans on their transactions to reaffirm our commitment to being the responsible choice. New customer acquisition focused on expanding the corporate cards portfolio.

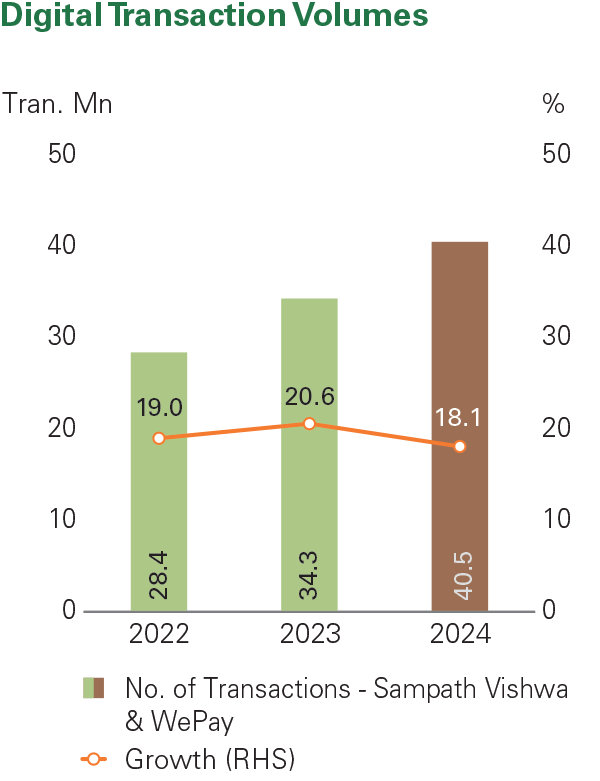

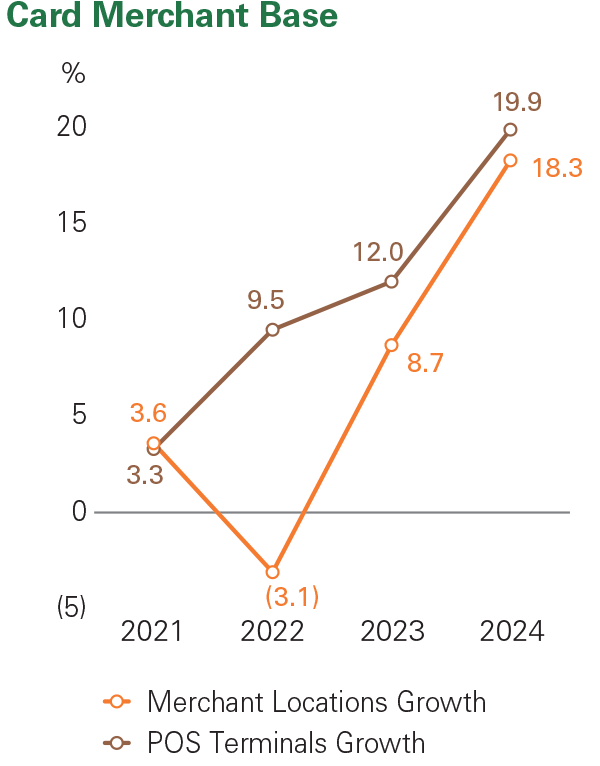

Cognisant of its role in supporting SME growth and the GOSL’s digitalisation efforts, the Unit pioneered the introduction of the mini-POS device in Sri Lanka in 2024. The bespoke, compact, portable device facilitates seamless transactions across multiple payment schemes, enabling the inclusion of SMEs into the digital payment system and expanding their revenue opportunities. During the year under review, over 640 SME merchants signed up for the mini-POS device, expanding their options for receiving payments while also facilitating greater payment ease for cardholders.

Given the rise in digital transactions and the risk of credit card frauds, the Card Centre engaged in numerous initiatives to raise public awareness in this regard. These included, SMS campaigns, e-flyers and island-wide merchant education programmes.

DEPOSITS

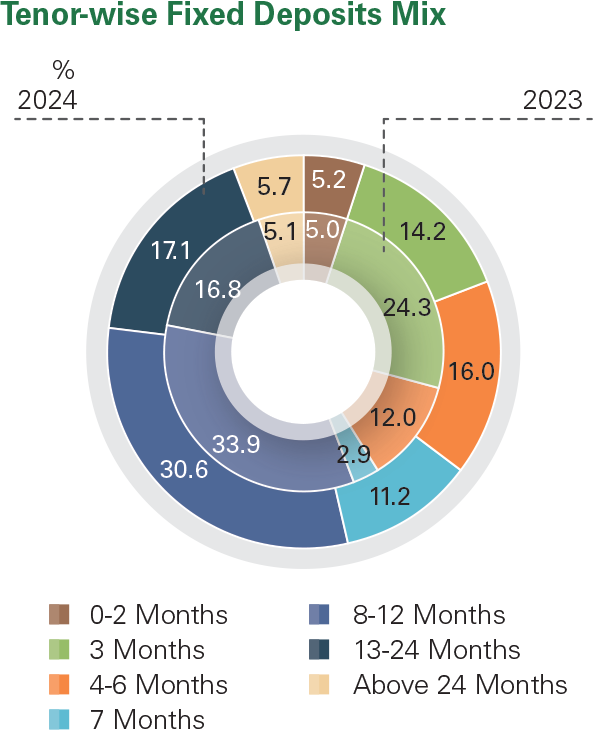

Despite declining interest rates, diminished disposable incomes and intense competition, the Bank’s deposit base recorded strong growth, expanding by 16.2% to Rs 1,469 Bn as at end-December 2024 (2023: 14.6% growth to Rs 1,264 Bn). Notably, emphasis on growing its low-cost funding base led to CASA growth outpacing term deposit expansion. Accordingly, CASA increased in proportion within the deposit mix to 34% while term deposits accounted for 65.5% as at end-December 2024.

The Bank’s robust deposit growth was underpinned by its strong brand and reputation, extensive island-wide reach with over 2,300 physical touchpoints, strong digital presence, and a diverse product range that caters to different life stages and needs of customers. Efforts to cross-sell deposit products across lending and transactional banking verticals, bundled service offerings to strategic partnerships, promotions, realignment of products to serve a variety of income and investment needs, prompt response towards adjusting the interest rates according to the market behaviours, intensified focus on deposit retention and superior service quality also played a significant role in driving deposit growth. Efforts to continuously evolve its product portfolio in line with customer needs resulted in the introduction of a new benefit scheme for Personal Foreign Currency Accountholders during the year, was executed with medical benefits, air fare reimbursement and data package offerings.

REMITTANCES

The increase in workers' remittances alongside strategic efforts to strengthen its presence in key markets and the provision of a superior value proposition to both remitters and beneficiaries underpinned the Remittance Unit’s strong performance and market position in 2024.

The Unit’s value proposition to remitters and beneficiaries centres on accessibility, speed, cost effectiveness and transparency. Accordingly, accessibility and convenience for overseas remitters were enhanced during the year under review, by expanding its global remittance partner network through the establishment of 10 new partnerships in key markets and strengthening relationships with its existing network of over 100 partners. To facilitate personalised service and strengthen brand visibility, the Unit also appointed two new overseas business promotion officers to Saudi Arabia and Oman in 2024. These efforts were supported by IT infrastructure that enabled instant transfer of funds to Sri Lanka from the country of origin and remittance tracking for both remitter and beneficiary. Remitted funds can be accessed by beneficiaries from over 2,300 touchpoints across the island or instantly transferred to the beneficiaries’ bank of choice enabling ease of access to beneficiaries. Efforts to promote account-based remittances amongst beneficiaries proved favourable, as the number of non-account-based beneficiaries continued to decline in 2024 as well. The year also saw many new initiatives to enhance operational efficiency. The Unit also launched a new payment system for remitters which enabled direct utility payments on behalf of beneficiaries as a new initiative to enhance convenience.

Building on the structural changes, IT investments and staff training initiatives implemented in 2024, the Unit intends to utilise the service efficiency and intensified SME focus derived from these efforts to more effectively capture emerging opportunities in the SME sector and strengthen its market position. The Unit also plans to continue to enhance its service proposition to SME and Retail customers through the introduction of new, customer-focused products and digital solutions.

Providing a unique and differentiated value proposition to customers alongside expanding and enhancing services to its merchant base will remain the Card Centre’s focus in the year ahead. To align with global trends and modernise its look and feel, the Unit also plans to re-design its credit cards. Plans are also underway to improve the Bank’s digital wallet WePay, through the launch of digital cards and innovative payment solutions.

The Deposits Unit intends to continue to develop innovative deposit products and related benefits that meet the evolving needs of its customers. In the year ahead, the Unit plans to double the medical benefit offered to Sanhinda Saver accountholders and introduce additional slabs to enhance eligibility of account holders for this benefit. Aligning with CBSL’s efforts to promote sustainable financing solutions, the Unit also plans to develop a green deposit product next year.

Meanwhile, the Remittances Unit plans to maintain its momentum in existing markets while continuously exploring new opportunities for growth. Emphasis will also be placed on continuing to evolve and enhance its value proposition to ensure superior service quality to both remitters and beneficiaries. The Unit also plans to leverage its partnerships with Fintechs to introduce innovative digital solutions that disrupt the remittance market.