CORPORATE GOVERNANCE REPORT

Sampath Bank recognises that strong Corporate Governance is the cornerstone of our long-term success, competitiveness, growth and most importantly, sustainability. While living up to its purpose as a leading private commercial bank in Sri Lanka, we are committed to upholding the highest standards of governance to ensure transparency, accountability and integrity in all our activities.

The Bank's Corporate Governance Framework is crafted to offer a solid structure that facilitates effective decision-making and oversight. Central to this framework are the integrated performance and conformance elements, which serve as its foundational pillars. This framework guides the Board of Directors in conscientiously fulfilling their fiduciary duties to fully meet stakeholder expectations. Moreover, the Governance Framework integrates regulatory requirements, voluntary codes and best practices, all of which are embedded within the Bank's internal policies and procedures. This combination serves as the foundation for fostering trust among all stakeholders including depositors and shareholders, while enhancing the Bank's reputation in the industry.

The Bank factoring the Listing Rules of the Colombo Stock Exchange (Listing Rules), the Banking Act Direction No. 11 of 2007 on Corporate Governance for Licensed Commercial Banks (Direction 2007) and the recently implemented Banking Act Direction No. 05 of 2024 on Corporate Governance for Licensed Banks (Direction 2024) reinforces the nexus to Sampath Bank's Corporate Governance Report. Additionally, the Bank also incorporated the best practices stipulated under the Code of Best Practice on Corporate Governance 2023 issued by the Institute of Chartered Accountants of Sri Lanka (Code 2023). Accordingly, we are pleased to report that the Bank has complied with the new requirements stipulated in Direction 2024, notwithstanding the stipulated deadlines, except for the extended deadlines which are given under ‘Way Forward’ of the Corporate Governance Report in page 183, while ensuring that the necessary steps are in place to adhere to the entire set of requisites of the aforementioned Direction 2024.

The Bank believes that Direction 2024 sets forth the essential guidelines and standards that constitute the core of our governance structure, upon which all governance principles rest, while Direction 2007, Listing Rules and Code 2023 further strengthen the foundation established by Direction 2024.

Above visual representation illustrates the synergy between foundational regulation and other driving rules that collectively inspire the Bank towards the true spirit of governance. In our pursuit for exemplary Corporate Governance, we envision a comprehensive framework that guarantees the integrity and effectiveness of the Bank's governance culture.

Corporate Governance should permeate every aspect of daily activities, extending beyond the confines of specific rules to shape the culture and ethics of the Bank. Through this Corporate Governance Report, Sampath Bank, an institution consistently striving to enhance its governance practices, demonstrates its genuine commitment to this objective by showcasing comprehensive governance compliance based on Direction 2024, Direction 2007, Listing Rules and Code 2023 as a collective approach, rather than taking individual regulations into consideration. Furthermore, we outline our governance practices, highlight key initiatives undertaken during the year under review and demonstrate Bank's unwavering commitment to ensure ethical conduct and corporate responsibility within the Bank's conduct. By fostering a culture of good governance, Sampath Bank aims to enhance its competitiveness, while assuring sustainable growth and contribute positively to the broader stakeholder groups.

We invite you to explore this report to gain a deeper understanding of the Bank's governance philosophy and the measures implemented to ensure the continued success and resilience of Sampath Bank PLC.

| Governance Framework | |||

|---|---|---|---|

| Regulatory Requirements | Internal Frameworks | Voluntary Codes and Best Practices | |

| The Companies Act No. 7 of 2007 and its amendments | Articles of Association | The Code of Best Practice on Corporate Governance 2023 issued by the Institute of Chartered Accountants of Sri Lanka | |

| The Banking Act No. 30 of 1988 and its amendments | Board approved Terms of Reference of Board and Board Sub-Committees | The Code of Best Practice on Corporate Governance 2017 issued by the Institute of Chartered Accountants of Sri Lanka | |

| Banking Act Direction No. 05 of 2024 on Corporate Governance for Licensed Banks | Board approved policy frameworks for governance, risk, compliance and operational areas | Global Reporting Initiative (GRI) Standards issued by the Global Sustainability Standards Board | |

| The Banking Act Direction No. 11 of 2007 on Corporate Governance for Licensed Commercial Banks issued by the Central Bank of Sri Lanka and its amendments | Codes of Conduct for Directors, Corporate Management and other Employees | The International Integrated Reporting <IR> Framework of the International Integrated Reporting Council (IIRC) | |

| The Anti-Money Laundering Laws and Regulations and Financial Transaction Reporting Act No. 6 of 2006 and its amendments | Preparer’s Guide to Integrated Reporting issued by the Institute of Chartered Accountants of Sri Lanka | ||

| The Listing Rules of the Colombo Stock Exchange | ISO 27001 Information Security Management | ||

| The Securities and Exchange Commission of Sri Lanka Act No. 36 of 1987 and its amendments thereto, as repealed by the Securities and Exchange Commission of Sri Lanka Act No. 19 of 2021 | United Nations Global Compact (UNGC) Sustainability Principles | ||

| The Inland Revenue Act No. 24 of 2017 and its amendments | International Labour Organisation (ILO) Convention for Social and Labour issues inducing Human Rights | ||

| The Shop and Office Employees Act No. 19 of 1954 and its amendments | United Nations Sustainable Development Goals (SDG) | ||

| The Sri Lanka Accounting and Auditing Standards Act No. 15 of 1995 | |||

| The Foreign Exchange Act No. 12 of 2017 and its regulations | |||

| The Code of Best Practices on Related Party Transactions issued by the Securities and Exchange Commission of Sri Lanka | |||

| Sri Lanka Accounting Standards issued by the Institute of Chartered Accountants of Sri Lanka | |||

| All other applicable regulations | |||

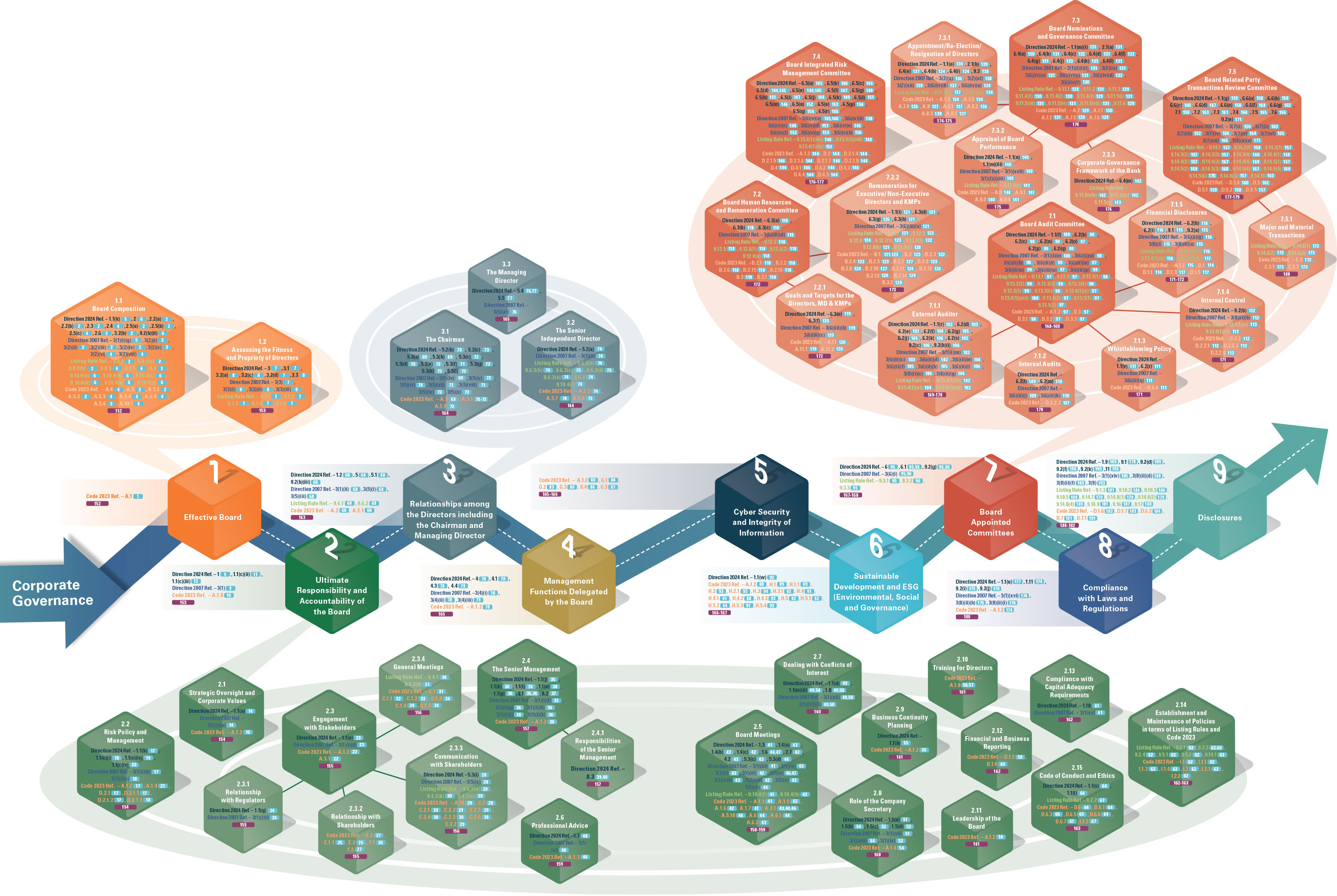

This fundamental approach forms the basis of Sampath Bank's Corporate Governance Report for 2024, highlighting the Bank's strong commitment to both mandatory and voluntary directions, rules and regulations. To elaborate on this approach, the diagram depicted herein provides a snapshot of the Bank's compliance status related to the Banking Act Direction No. 05 of 2024 on Corporate Governance for Licensed Banks (Direction 2024), Banking Act Direction No. 11 of 2007 on Corporate Governance for Licensed Commercial Banks (Direction 2007), Listing Rules of the Colombo Stock Exchange (Listing Rules) and Code of Best Practice on Corporate Governance 2023 issued by the Institute of Chartered Accountants of Sri Lanka (Code 2023), along with a detailed description.

As a result, the Corporate Governance Report is structured into nine (09) main topics, with certain topics further divided into sub-topics as appropriate which are highlighted in distinct colours. Each square indicates the relevant topic name along with the governance requirements outlined in Direction 2024, Direction 2007, Listing Rules and Code 2023.

denotes the exact paragraph number demonstrating compliance status for the specific section or governance requirement, while indicates the page number(s) where the relevant descriptions can be found.

Accordingly, we affirm that the Bank has fully complied with the Corporate Governance requirements under the Direction 2024, Direction 2007, Listing Rules and Code 2023 as applicable for the reporting period.

1) EFFECTIVE BOARD

Code 2023 Ref. - A.1

Sampath Bank PLC (The Bank) has an effective Board committed to fulfilling its function in accordance with laws, regulations and good governance practices. Further, Directors are regularly briefed on regulatory developments during Board Meetings to ensure that their knowledge remains up-to-date, enabling them to discharge their responsibilities effectively.

1.1 BOARD COMPOSITION

Direction 2024 Ref. - 1.1(k), 2, 2.2(a), 2.2(b), 2.3, 2.4, 2.5(a), 2.5(b), 2.5(c), 2.6, 3.2(b), 9.2(h)(ii)

Direction 2007 Ref. - 3(1)(i)(g), 3(2)(i), 3(2)(ii), 3(2)(iii), 3(2)(iv), 3(2)(v), 3(2)(vi), 3(2)(viii)

Listing Rule Ref. - 9.8.1, 9.8.2(a), 9.8.2(b), 9.8.3, 9.8.5, 9.9, 9.10.4(a), 9.10.4(b), 9.10.4(c), 9.10.4(d), 9.10.4(e), 9.10.4(g)

Code 2023 Ref. - A.4, A.5, A.5.1, A.5.2, A.5.3, A.5.4, A.5.5, A.5.6, A.10.1

The Bank is led by a competent and well-balanced Board of Directors. The Sampath Bank Board as at 31st December 2024 comprised eleven (11) Directors, including two (02) Executive Directors (EDs) and nine (09) Non-Executive Directors (NEDs). Out of the nine (09) NEDs, seven (07) are Independent Directors (INDs). There were no changes made to the minimum ratio of the INDs as stipulated in the regulations during the year 2024. Accordingly, the current Board composition fulfils all specified regulatory compliance requirements pertaining to Board Balance as detailed below:

- Direction 2007 stating that the number of NEDs should not be less than 1/3 of the total number of Directors of the Board;

- Direction 2007 and 2024 stating that the number of EDs shall not exceed 1/3 of the total number of Directors of the Board;

- Direction 2024 stating that the number of Independent, NEDs shall not be less than 1/2 of the total number of Directors of the Board;

- Listing Rules stating that the number of INDs should not be less than 1/3 of the total number of Directors of the Board;

- Code 2023 which prescribes that 2/3 of NEDs of the Board should be independent.

The appointment of Alternate Directors to represent Directors at Board meetings can be done where necessary in line with the Board approved policy subject to relevant regulatory requirements and approvals. However, there were no Alternate Directors appointed during the year 2024.

The NEDs of the Bank are personnel with credible track records of good conduct, integrity and have necessary knowledge, skills and

experience to bring an independent judgement to effectively address issues of strategy, performance, resources and to contribute

towards the sustainability of the Bank. The Independent Directors are free of any business or other relationship that could materially

interfere with the exercise of their unfettered and independent judgement. Each NED submits declarations confirming his/her

independence or non-independence each year against the specified criteria to conduct evaluations on the independence of the

Directors based on such declarations. The Independent, NEDs are expressly identified by specifying their individual directorship

status in all corporate communications that disclose the names of Directors of the Bank. No Independent Director impaired his/her

independence as set out in the relevant regulatory requirements during the year under review.

Furthermore, the Bank requires to submit declarations by the Independent, NEDs confirming their status of independence for

quarterly evaluations by the Board Nominations and Governance Committee (BNGC), taking into account the new requirement

effective from 1st January 2025. Accordingly, any changes to the independent status (if any) will be notified to the regulatory

authorities.

The Board has defined the areas of authority and key responsibilities of the Directors in the "Policy on Internal Code of Business Conduct and Ethics for Directors" and the Terms of Reference (TOR) of the Main Board. The Board of Directors has delivered the entrusted responsibilities at an optimum level under the defined areas of authority during the year under review.

The Board diversity demonstrated on page 197 of the Board Nominations and Governance Committee Report whereas the profiles of Directors detailing their qualifications, expertise, Executive/Non-Executive and Independent/Non-Independent status, memberships in Board Sub-Committees, Companies and other entities in which each Director serves as a Board member along with their key appointments are disclosed on pages 186 to 189. The details of immediate family and/or material business relationships with other Directors of the Bank are given in Annual Report of the Board of Directors on the Affairs of the Company on pages 255 to 263. As described in the pages 186 to 189, it is evident that a majority of Directors possess sufficient Financial Acumen within the Board on matters of finance. Further, information pertaining to the Directors are disclosed in the following reports:

- Related Party Transactions are given on pages 363 to 366 (Note 47);

- Directors' Interests in Contracts are given on pages 262 and 263;

- Director's attendance at Board Meetings and Board Sub-Committee meetings are given on page 158.

1.2 ASSESSING THE FITNESS AND PROPRIETY OF DIRECTORS

Direction 2024 Ref. - 3, 3.1, 3.2(a), 3.2(c), 3.2(d), 3.3

Direction 2007 Ref. - 3(3), 3(3)(i), 3(3)(ii), 3(3)(iii)

Listing Rule Ref. - 9.7.1, 9.7.2, 9.7.3, 9.7.4, 9.7.5

The Fitness and Propriety of Directors are prudently assessed by the BNGC when considering appointments to the Board and during the annual assessment of continuation of directorships in order to strengthen the diversity of the Board to induce fresh perspective that will foster robust debate and support effective decision-making. The BNGC ensures that the Directors and the Managing Director (MD) are being adequately assessed according to the Fit and Proper Assessment Criteria that has been defined in the relevant regulations applicable for the same. The Bank obtained annual declarations from the Directors confirming that they have continuously satisfied the specified Fit and Proper Assessment Criteria and no failures reported during the year under review. Further, when considering appointments to the Board and during the annual assessment of continuation of directorships, the BNGC ensures that the respective Directors have sufficient time to carry out the responsibilities as a Director of the Bank.

In compliance with the Direction 2007 and 2024, none of the Directors in the Board exceeds the age of 70 years. Further, none of the Directors hold directorships of more than twenty (20) companies/entities/institutions inclusive of Subsidiary Companies of the Bank. The Bank has complied fully with the directions applicable for the mandatory cooling-off period when appointing new Directors to the Board during the year under review.

2) ULTIMATE RESPONSIBILITY AND ACCOUNTABILITY OF THE BOARD

Direction 2024 Ref. - 1, 1.1(c)(ii), 1.1(c)(iii)

Direction 2007 Ref. - 3(1)

Code 2023 Ref. - A.1.8

The Board bears the ultimate responsibility and accountability for overseeing the management of the Bank's affairs, governance framework, business strategy, financial soundness and risk management. The Board ensures that the Bank's operations comply with all applicable laws and regulations and align with sound banking practices. Directors make decisions objectively, prioritising the interests of depositors, creditors, shareholders and other stakeholders whereas any decisions made by the Directors are presumed to be collective decisions of the Board, except when a Director expressly dissents.

When accepting the appointment as a Director of the Bank, Directors ensure that they have meticulously considered the responsibilities associated with the role, their ability to dedicate the adequate time, any existing or potential conflicts of interest and the competencies required for the position.

In alignment with Bank's commitment to robust risk governance, the Bank has successfully established well-defined organisational responsibilities across the three lines of defence within the organisation. The business lines are tasked with the initial management of risks, ensuring that risk-taking activities are conducted within the established risk appetite. The risk management and compliance functions operate independently from the business lines and internal audit, providing a second layer of oversight and ensuring adherence to regulatory requirements and internal policies. Furthermore, Bank's internal audit function, which is independent from both the business lines and the risk management and compliance functions, conducts regular reviews to ensure the effectiveness of the risk management framework. This structured approach reinforces the Bank's dedication to maintaining a strong risk governance culture and ensures comprehensive risk oversight across all levels of the organisation.

The risk management, compliance and internal audit functions are properly positioned, sufficiently staffed and resourced to carry out their responsibilities independently, objectively and effectively. This ensures the highest standards of governance and integrity are maintained, with operations conducted in a manner that mitigates risks and adheres to all relevant regulations. This approach strengthens organisational resilience and enhances the ability to achieve strategic objectives with confidence.

The Board of Directors, as the highest governing body of the Bank, plays a pivotal role in demonstrating good corporate citizenship, ethical behaviour, transparency and accountability. In its capacity as the main custodian of the Bank, the following matters are expressly reserved for Board consideration.

2.1 STRATEGIC OVERSIGHT AND CORPORATE VALUES

Direction 2024 Ref. - 1.1(a)

Direction 2007 Ref. - 3(1)(i)(a)

Code 2023 Ref. - A.1.2

The Board formulates the Bank's Purpose, Vision, Corporate Values, Strategic Objectives and provides oversight and direction to ensure that the management and all employees work towards the said Vision. The Board Strategic Planning Committee (BSPC) ensures that the revolving Strategic Plan relevant for each year is reviewed on a periodic basis, in order to facilitate strategic realignment wherever and whenever deemed necessary or as appropriate. The review and approval of the Strategic Plan includes the medium-term and short-term targets and the annual budgets with a special emphasis to the scale and complexity of the business operations. The Bank's Strategic Objectives and Corporate Values are communicated to all levels of staff through regular briefing sessions and reinforced by the Corporate Management Team. The Strategic Objectives and Corporate Values are also conveyed to new recruits as a part of their Induction Programme and are given on pages 43 and 10 respectively of this Annual Report.

Taking a quantum leap in its strategic planning process, the Board engaged the expertise of a leading global consultancy firm in 2023 to develop a five (05) year Strategic Plan for the Bank. This strategic planning process involved extensive analysis of internal and external factors such as local and international economic/business environment, opportunities, technology, risks and compliance etc. in collaboration with all stakeholders. The budgets, including major capital expenditure items and revolving Strategic Plan for 2024 onwards were duly approved by the Board in compliance with the statutory requirements. The Strategic Plan is now being implemented over the period 2024-2028 under the guidance of the Board, with adequate provisions for short and medium-term exigencies induced by the external environment.

Prior to approving the Strategic Plan and the Annual Budget, the Board collaborated with relevant Board Sub-Committees, the Corporate Management Team, the Strategic Planning Department, the Risk Management Unit and the Compliance Department to weight the risks and opportunities. The Board also undertakes to monitor the Bank's performance vis-à-vis the Strategic Plan and budget on a quarterly basis, taking into account the underlying downside risks associated with the macro-economic variables.

2.2 RISK POLICY AND MANAGEMENT

Direction 2024 Ref. - 1.1(b), 1.1(c)(i), 1.1(c)(iv), 1.1(c)(v)

Direction 2007 Ref. - 3(1)(i)(b), 3(1)(i)(c)

Code 2023 Ref. - A.1.2, A.1.4, D.2.1, D.2.1.1, D.2.1.2, D.2.1.3

The revolving Strategic Plan for the period 2024-2028 approved by the Board during 2023 in consultation with the Corporate Management was successfully implemented with regular reviews. In addition, the Risk Management Framework and mechanisms have also been approved by the Board in line with the Strategic Plan 2024-2028. Measurable goals for the Bank as a whole have been set with performance milestones that were measured quarterly during 2024.

The Board Integrated Risk Management Committee (BIRMC) is responsible for independently reviewing, identifying, measuring, monitoring and controlling all the risks. To ensure this process, the BIRMC is tasked with recommending the Bank's risk policies, defining the risk appetite, identifying principal risks, setting risk governance structures and implementing systems to measure, monitor and manage the principal risks prudently. The BIRMC is under the purview of the Main Board and responsible for updating significant risk events to the Main Board. The following reports provide further insights in this regard and contain the information pertaining to material foreseeable risk factors of the Bank.

- Risk Management Report is given on pages 224 to 251.

- Board Integrated Risk Management Committee Report is given on pages 204 to 206.

Defining the risk appetite of the Bank aligning with the Bank's strategic, capital and financial plans is done by the BIRMC and approved by the Board. This is reflected in the Board approved Risk appetite statement. The Risk Appetite Limits and Key Risk Indicators of the Bank are monitored on a regular basis.

The BIRMC takes prompt corrective action to mitigate the effects of specific risks in case such risks are at levels beyond the prudent risk levels decided by BIRMC based on the Bank's policies, regulatory and supervisory requirements. The BIRMC refers to the Human Resources Department in respect of the officers identified to be responsible for failure to identify specific risks in order to take prompt corrective actions as directed.

An insurance policy is in place in line with the regulatory requirements to cover the Board of Directors and officers including Key Management Personnel (KMPs) of the Bank. The adequacy and effectiveness of the insurance covers are reviewed periodically with the assistance of external expertise.

2.3 ENGAGEMENT WITH STAKEHOLDERS

Direction 2024 Ref. - 1.1(e)

Direction 2007 Ref. - 3(1)(i)(d)

Code 2023 Ref. - A.1.2, A.3.1

It is the fundamental duty of the Board to protect the interests of all stakeholders including shareholders, customers, employees, regulators and the wider community by exercising appropriate control to ensure the Bank is managed effectively in order to meet stakeholder deliverables. The Bank's Articles of Association empowers the Board to make decisions to protect the interests of all stakeholders. In addition, the Customer Charter, the Bank’s HR Policy Manual, the "Policy on Managing Conflicts of Interest", the Board Shareholder Relations Committee (BSRC) as well as the Board Related Party Transactions Review Committee (BRPTRC) together create a fully-fledged ecosystem to uphold the interests of all stakeholders.

Well aware of its responsibility to stakeholders, the Board engages directly with employees, customers, regulators and shareholders from time to time. For this purpose, a Board approved "Policy on Communication" is in place and serves as the basis for communicating with all stakeholders, including depositors, creditors, shareholders and borrowers. Refer pages 49 to 56 for further details on "Engaging with Our Stakeholders".

2.3.1 Relationship with Regulators

Direction 2024 Ref. - 1.1(q)

Direction 2007 Ref. - 3(1)(i)(l)

To demonstrate its dedication to good governance, the Bank has consistently fostered strong relationships with regulators. The MD or an appointed representative attends all scheduled CEO/MD forums on governance organised by the Central Bank of Sri Lanka (CBSL). Additionally, the Board of Directors and relevant officers participate in meetings and special events convened by the regulators, including the CBSL, as applicable.

2.3.2 Relationship with Shareholders

Code 2023 Ref. - E.1, E.1.1, E.2, F.1, F.2

The Board executes its responsibility to shareholders by encouraging their participation in the decision-making process through the provision of fair and transparent disclosures. The Bank's Institutional Investors as well as other Investors have throughout exercised their votes enthusiastically, expressing candid preferences and are encouraged to express their views freely. The Bank has a history of active shareholder involvement and participation at general meetings. The Bank is proud to announce that the Board Sub-Committee on Shareholder Relations, established in 2008, successfully held the Shareholder Relations Forum following the 38th Annual General Meeting (AGM) on 28th March 2024 with the aim of maintaining a solid and productive dialogue with shareholders ensuring their views are communicated to the Board. Further, Institutional Investors are kept apprised of the Bank's governance practices through the Annual Report and any new initiatives are highlighted at general meetings to ensure that due weightage is given to good Corporate Governance.

The Annual Report contains sufficient information for individual shareholders as well as for all potential Investors to carry out their own analysis. This, together with the interim financial statements published each quarter provides sufficient information to enable individual shareholders to make informed judgements regarding the Bank's performance and future prospects. Additionally, a separate part of the Bank's corporate website (www.sampath.lk) is dedicated to Investor Relations, which provides relevant information online to all Investors. Shareholders can contact the Company Secretary for further information if required. Meanwhile, circulars issued to shareholders from time to time emphasize the importance of making independent decisions prior to initiating any particular investment.

It is a tradition at the Bank to encourage individual shareholders to participate and vote at any general meetings. Additionally, they are encouraged to participate in the Bank's affairs by submitting proposals through the Stakeholder Feedback Form attached with the Annual Report. The general meetings also serve as a platform for the Bank to engage with its shareholders. Sampath Bank has a proud history of well-attended general meetings where shareholders take an active role in exercising their rights in all forms.

2.3.3 Communication with Shareholders

Direction 2024 Ref. - 5.3(i)

Direction 2007 Ref. - 3(5)(x)

Listing Rule Ref. - 9.4.2(a), 9.4.2(b), 9.4.2(c)

Code 2023 Ref. - A.10, C.2, C.2.1, C.2.2, C.2.3, C.2.4, C.2.5, C.2.6, C.2.7

The Chairman and the Board of Directors ensure that appropriate steps are taken to maintain effective communication with shareholders and that the views of shareholders are communicated to the Board of Directors through the BSRC.

The Bank's Annual Report, Interim Financial Statements and other materials are available for download on its corporate website. These documents are posted promptly after being released to the CSE. Public disclosures are promptly shared with shareholders via market announcements. The Bank ensures fair and transparent disclosures, focusing on integrity, accuracy, timeliness, and relevance. The Board-approved "Policy on Communication" and “Policy on Relations with Shareholders and Investors” outline shareholder communication requirements. Responsibilities for stakeholder communication are defined in the policy implementation mechanism under each Policy.

Shareholders are duly notified that any communication/correspondence with the Bank should be through the Company Secretary. They may provide their concerns and suggestions to the Directors or Management through the Company Secretary. The contact information of the Company Secretary is provided in the Annual Report and the Bank’s corporate website. Additionally, shareholders are at liberty even to communicate directly with any of the Board Members. They may, at any time, direct questions or request publicly available information from the Directors or Management of the Bank. The Company Secretary takes appropriate action based on the concerns/requests received from the shareholders and communicates the appropriate decisions formulated by the Board. Further, shareholders are kept advised of relevant details in respect of Directors as and when required.

2.3.4 General Meetings

Listing Rule Ref. - 9.4.1, 9.4.2(d)

Code 2023 Ref. - C.1, C.1.1, C.1.2, C.1.3, C.1.4, C.1.5

General meetings provide an opportunity for shareholders to engage directly with the Board and the Management.

The Bank consistently promotes conducting these meetings in person in almost every opportunity. The AGM is the main forum

to interact between the shareholders and the Board and create an opportunity for shareholders for their views to be heard. The

38th AGM was held physically at “Balmoral”, the Kingsbury on 28th March 2024. The Chairpersons of all mandatory Board Sub-

Committees and the Senior Independent Director were available to answer questions if so, requested by the Chairman.

Additionally, during the year under review, the Bank convened two (02) Extraordinary General Meetings (EGMs) on 28th March 2024

and 23rd December 2024 to secure the approval of the shareholders:

- for the amendments to the Bank's Articles of Association (as a physical meeting)

- for the proposed BASEL III compliant debenture issue (as an online-virtual meeting).

The notice of the AGM and the other papers related thereto, are duly circulated to all shareholders fifteen (15) working days prior to the AGM. The notices of other General Meetings were also duly circulated to all shareholders within the timelines stipulated by the statutes.

During the AGMs, separate resolutions are proposed and adopted on each substantial issue including the adoption of the Annual Report of the Board of Directors on the Affairs of the Company and the statements of the Audited Accounts for the year under review. All proxy votes lodged, together with the votes of shareholders who participated at the AGM are considered for each resolution. The votes withheld are not considered in determining the number of votes for and against each resolution.

The Bank duly maintains a register to ensure that all valid proxies received in respect of the general meetings are properly recorded and counted. The register is closed on the proxy submission deadline specified in the notice of meeting. The number of votes received in favour, against and abstaining on each resolution are announced at the relevant General Meeting and also the records are maintained properly by the Bank as per regulatory requirements. At the meeting, for adoption of each resolution, the Chairman, in addition to the details of the proxies registered, calls for a vote in line with the established practices followed by the announcement, as to whether the resolution is carried or not. A summary of the procedure governing voting at General Meetings is properly briefed to the shareholders at the respective General Meetings.

2.4 THE SENIOR MANAGEMENT

Direction 2024 Ref. - 1.1(j), 1.1(k), 1.1(l), 1.1(o), 1.1(p), 8.1, 8.2

Direction 2007 Ref. - 3(1)(i)(f), 3(1)(i)(g), 3(1)(i)(h), 3(1)(i)(j), 3(1)(i)(k)

Code 2023 Ref. - A.1.2

In terms of Direction 2024 the Senior Management includes the CEO and the KMPs of the Bank. The Bank has identified KMPs as persons in positions that can significantly influence policies, direct activities and exercise control over business activities, operations and risk management of the Bank. Accordingly, the Board has identified the members of Corporate Management including the MD, the Chief Compliance Officer and the Assistant Company Secretary as KMPs who represent the Senior Management of the Bank.

The Board has outlined the areas of authority and key responsibilities for the KMPs which are detailed in their individual Position Descriptions. The KMPs have delivered the entrusted responsibilities at an optimum level under the defined areas of authority that is consistent with the Board's strategies and policies throughout the year under review. The KMPs are called upon as and when required to attend meetings of the Board and its Sub-Committees to review policies, establish communication lines and other matters relating to the scope of work under their respective purview to monitor progress towards achieving corporate objectives. The KMPs may also be required to make regular presentations to the Board as appropriate. The Board ensures that the MD and the Corporate Management possess the necessary skills, collective knowledge and expertise given the size, scale, diversity and complexity of operations which are required to implement the strategy of the Bank.

In terms of regulatory requirements, the BNGC evaluated and identified that the members of the Senior Management fulfil the criteria for fitness and propriety, ensuring that each individual discharges their duties effectively.

The Bank develops and updates succession plans for the KMPs aligned to the Bank’s strategic objectives to ensure at least one successor is identified for each role. A Board approved succession plan for Corporate Management is in place.

2.4.1 Responsibilities of the Senior Management

Direction 2024 Ref. - 8.3

The Senior Management ensures that they,

- contribute substantially to the Bank's sound corporate governance framework through personal conduct;

- devote sufficient professional time to discharge their duties;

- implement business strategies, risk management systems, risk and compliance culture, processes and controls for managing both financial and non-financial risks in terms of the directions of the Board;

- recognise and respect the independent duties of the risk management, compliance and internal audit functions and shall not interfere in the exercise of such duties;

- receive access to regular training to maintain and enhance competencies and keep abreast of developments relevant to the respective areas of responsibility;

- are responsible for delegating duties to staff and overseeing such delegated duties;

- establish a management structure that promotes Bank-wide accountability and transparency;

- take appropriate remedial or disciplinary action if any breaches are identified;

- regularly provide the Board and the Board Sub-committees as applicable with the information of material matters including but

not limited to;

- changes in business strategy, risk strategy/risk appetite,

- performance and financial condition,

- breaches of risk limits or compliance rules,

- internal control failures,

- legal or regulatory concerns;

- notify the Director of Bank Supervision upon becoming aware of any material information that may negatively affect the fitness and propriety of a Board member or another Senior Management member.

Recognising the importance of good governance, the Senior Management proactively fulfilled the above requirements set to take effect on 01st January 2025. This forward-thinking approach underscores the Bank's dedication to best practices and unwavering commitment to corporate integrity, as evident from the explanations provided throughout this Annual Report.

2.5 BOARD MEETINGS

Direction 2024 Ref. - 1.3, 1.4(a), 1.4(b), 1.4(c), 1.6, 2.7, 4.2, 5.3(c), 5.3(d)

Direction 2007 Ref. - 3(1)(iii), 3(1)(iv), 3(1)(v), 3(1)(vi), 3(1)(x), 3(1)(xiii), 3(2)(vii), 3(5)(v), 3(5)(vi)

Listing Rule Ref. - 9.10.4(f), 9.10.4(h)

Code 2023 Ref. - A.1.1, A.1.5, A.1.6, A.1.7, A.3.1, A.5.10, A.6, A.6.1, A.6.2

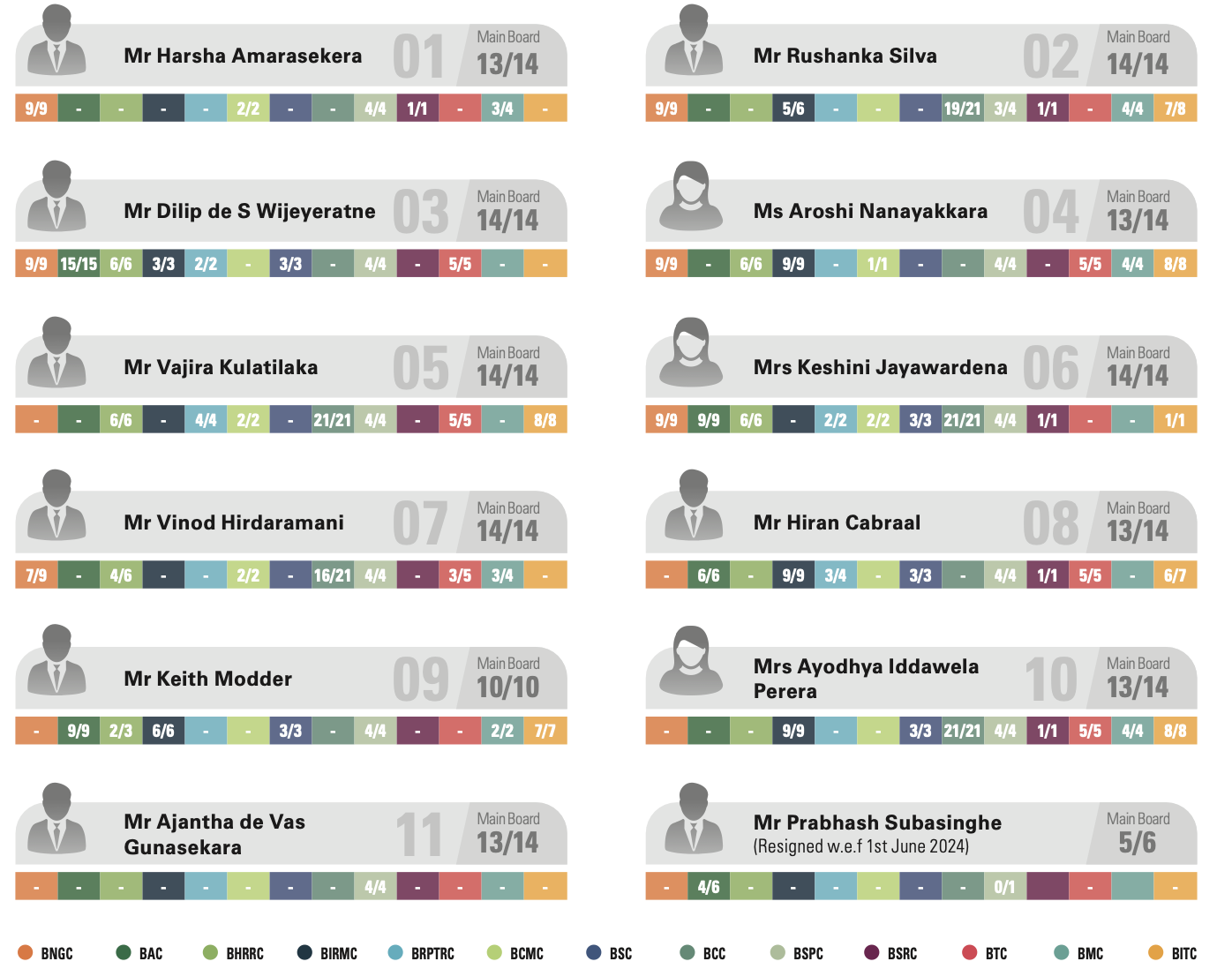

Regular Board Meetings are held whereas special meetings are scheduled on need basis and the Board met fourteen (14) times during 2024. Such regular Board Meetings necessarily involve active participation in person of a majority of Directors entitled to be present. The Bank has minimised obtaining approval via circulation of written resolutions/papers and it is done only on an exceptional basis. The approvals obtained via circulation were ratified at the Board meetings held immediately following the circulation. Additionally, resources are in place enabling members to virtually participate in Board meetings, fostering active engagement and ensuring seamless communication across all locations. During the year under review, the Board ensured that the majority of its members regularly attended Board meetings in person and Directors who joined the meetings virtually under exceptional circumstances attended in person at least on a half-yearly basis, in compliance with regulatory requirements.

Every Director commits sufficient time to Board matters. Directors who are members of respective Board Sub-Committees are dedicated to their responsibilities. All Directors attended at least 2/3 of the Board Meetings and no Director was absent from three consecutive meetings during the year under review. More than 1/2 of the Board members were present at each meeting, constituting the quorum for Board Meetings conducted in the year 2024. Further, more than 1/3 of the independent, NEDs were present at each meeting. During the year under review, in discharging the duties the Directors exercised independent judgment in strategy, performance, resource allocation, risk management, compliance and standards of business conduct.

DIRECTORS' ATTENDANCE AT BOARD AND BOARD SUB-COMMITTEE MEETINGS (ATTENDED/ELIGIBLE TO ATTEND)

Dates of regular Board Meetings and Board Sub-Committee Meetings are scheduled well in advance and the notice of meetings, the relevant meeting agenda along with the respective papers are generally circulated seven (07) days prior to the meeting by uploading the same via a secure link, providing Directors an opportunity to get prepared and attend the same. There is a provision to circulate urgent papers closer to the meeting on an exceptional basis. Further, minutes of the meetings are generally provided within the stipulated period. The routine agenda for Board Meetings is developed by the Chairman in consultation with all other Directors and the Company Secretary taking into consideration matters relating to the Board Meeting covering all-important areas under discussion. A Board approved procedure is in place to permit any Director to include any matter or proposal in the Board and/or in a Sub-Committee Meeting agenda especially where such matters and proposals relate to the promotion of banking business, risk management and conduct of employees of the Bank. Further, a Board approved "Policy on Matters Relating to Board of Directors" is in place specifically reserving for its decision to ensure that the direction and control of the Bank is within its authority in line with regulatory guidelines and international best practices.

The Board has access to comprehensive, quantitative and qualitative information needed to enable them to effectively discharge their duties. The Management provides comprehensive information to Directors during the monthly Board Meetings. Board papers are informative and any further information required by Directors is provided by the Management, upon request. A Board approved procedure is in place enabling all Directors to request inclusion of matters of concern in the agenda while all Directors have access to KMPs should they need to seek information for discussions at Board Meetings. Further, the Chairman ensures that the Board is adequately briefed and informed regarding matters arising at Board Meetings in a timely manner. The following processes are in place to ensure the same.

- Agenda and Board papers are circulated with adequate time for the Directors to go through the same.

- Relevant members of the Management Team are available for explanations and clarifications if required.

- Management information is provided in agreed formats on a regular basis to enable Directors to assess the performance and stability of the Bank.

Any Director who was unable to attend a meeting is updated on proceedings prior to the next meeting through:

- formally documented minutes of meetings;

- a separate document on matters arising out of minutes highlighting the items which need to be completed and need follow-up actions of the previous meetings (This is taken up immediately after confirmation of minutes);

- archived minutes and Board papers accessible electronically at the convenience of the Directors.

The minutes of Board and Board Sub-Committee Meetings carry important concerns raised and views expressed by Directors individually to highlight how the Board has arrived at the decision in the deliberations as precisely as possible. When preparing minutes of the proceedings of a meeting the concerns raised by each Director are clearly recorded together with the responses of the other, which are important for the final decision of the Board.

The detailed minutes of the meetings include the following:

- a summary of data and information used by the Board in its deliberations;

- the matters considered by the Board members;

- the fact-finding discussions and the issues of contention or dissent;

- the testimonies and confirmations of relevant KMPs which indicates compliance with the Board’s strategies and policies and adherence to relevant laws and regulations;

- matters related to risks to which the Bank is exposed and an overview of the risk management measures adopted;

- the decisions and resolutions of Board/Board Sub-Committees.

2.6 PROFESSIONAL ADVICE

Direction 2024 Ref. - 1.7

Direction 2007 Ref. - 3(1)(xi)

Code 2023 Ref. - A.1.3

A Board approved policy has been established to enable Directors to seek Independent Professional Advice in appropriate circumstances at the Bank's expense. This facility is coordinated through the Company Secretary with the approval of the Board Chairman to assist the relevant Director/s to discharge his/her/their duties to the Bank.

2.7 DEALING WITH CONFLICTS OF INTEREST

Direction 2024 Ref. - 1.1(d), 1.1(m)(ii), 1.8

Direction 2007 Ref. - 3(1)(xii), 3(1)(i)(i)(ii)

The Directors at all times take necessary steps to avoid conflicts of interest or the potential conflicts of interest,

in their activities with and commitments to, other organisations, Related Parties and other stakeholders. The Directors are also

conscious of their obligation to deal with situations where there is a conflict of interest in accordance with the Bank’s "Policy on

Managing Conflicts of Interest" and the Directions 2007 and 2024. This Policy has been developed in line with applicable regulatory

requirements and best practices and its effectiveness is periodically reviewed by the Board.

The "Policy on Managing Conflicts of Interest" ensures that the Board is not dominated or significantly influenced by a Director or a

group of Directors in a manner that is detrimental or prejudicial to the interests of the depositors, creditors and the Bank as a whole.

As per the Policy, where there is deemed to be a conflict of interest either in respect of the Director, his/her close relation or a

concern in which he/she has substantial interest, is interested, the respective Directors refrain from participating in the discussions,

voicing their opinion, approving the same and accessing the information pertaining thereto, physically and/or electronically. Such

actions are appropriately minuted for future reference and the Director concerned is not counted in the quorum in such instances.

In addition, "Policy on Anti-Bribery and Corruption" and relevant internal guidelines are in place to ensure the Bank's commitment

towards anti-corruption practices. Further, an effective and comprehensive internal control framework for identifying, recording and

disclosing Related Party Transactions is also in place.

The Directors annually confirm that there are no relationships between the Directors among themselves and as well as between the

Directors, MD and KMPs are at a level that does not result in excessive familiarity, undue influence or coercion.

The Bank regularly updates the Register of Directors' Interests to meet regulatory requirements.

2.8 ROLE OF THE COMPANY SECRETARY

Direction 2024 Ref. - 1.5(a), 1.5(b), 1.5(c), 1.5(d)

Direction 2007 Ref. - 3(1)(vii), 3(1)(viii), 3(1)(ix)

Direction 2007 Ref. - A.1.4

The appointment of the Company Secretary is governed by the provisions of Section 43 of the Banking Act No. 30 of 1988. Accordingly, the Board has appointed a Company Secretary who is an Attorney-at-Law of the Supreme Court of Sri Lanka to oversee secretarial services for the Board Meetings and shareholder meetings and to carry out other functions as specified in the statues and other regulations. The Articles of Association of the Bank specifies the conditions for the appointment and removal of the Company Secretary.

The Company Secretary is a member of the Corporate Management Team and is considered to be a part of the KMPs of the Bank. The main role of the Company Secretary is to guide the Board on discharging its duties and responsibilities, by promoting Corporate Governance best practices and informing the Board of relevant legislative and regulatory changes applicable to the same. The Company Secretary is accountable to the Board for maintaining the minutes of the Board Meetings and circulating the same among all Board Members. It is the responsibility of the Company Secretary to allow Directors to access past Board papers and minutes through the secure electronic link via iPads. Additionally, the minutes of the Board meetings are available for inspection by the Regulator at any reasonable time with reasonable notice. Further, the Company Secretary is required to make sure Directors are briefed on developments in the regulatory environment at Board Meetings to ensure that their knowledge is updated regularly to discharge their responsibilities effectively.

The Company Secretary implements the recommendations of the BNGC relating to training, capacity building and professional development programmes for the Directors.

A Board approved policy is in place, ensuring that all members of the Board have the opportunity to obtain advice and services of the Company Secretary with regard to the compliance with relevant rules, regulations, directions and statutes.

2.9 BUSINESS CONTINUITY PLANNING

Direction 2024 Ref. - 1.1(h)

Code 2023 Ref. - A.1.2

The Board remains the ultimate authority in charge of ensuring the continuity of business operations to support the going concern principle. For this purpose, a Board approved Business Continuity Plan (BCP) is in place. The BCP is reviewed and updated annually or more often if needed in cognisance with contextual changes in the internal and external operating environment, with Board approval sought for any material updates to the BCP. Under the BCP testing protocols for 2024, the Disaster Recovery (DR) Drill was conducted for an extended period of time to ensure operational resilience and preserve critical operations and services. During the Drill, all operating systems including core-banking systems were functioned through DR Servers. Moreover, a series of system simulations were conducted to measure system resilience against the worst-case scenario. The Bank has developed delegated DR Sites for all critical functions of the Bank and the delegated DR Sites were also tested quarterly to ensure proper functioning of sites as well as familiarisation of team members. With the aim of ensuring safety of occupants of the building, training on “Fire Safety and Emergency Evacuation” and Fire Drill/Evacuation Drill were also conducted.

2.10 TRAINING FOR DIRECTORS

Code 2023 Ref. - A.1.8

Given the stewardship role undertaken by the Board, it is vital that all Directors remain relevant and up-to-date in terms of the skills and knowledge needed to carry out their roles and responsibilities as well as to perform their fiduciary duties as Board of Directors. Accordingly, the Directors consistently demonstrate a strong commitment to enhance their knowledge and are provided with access to learning, development and training opportunities that align with the latest developments in applicable laws, regulations, macroeconomic policies, the latest technological developments, emerging financial sector and market developments and all other areas relevant to banking industry. The BNGC, in consultation with the Board of Directors, recommends appropriate training sessions/seminars/workshops for Directors. The annual self-assessment by Directors also serves as an important source for identifying the training needs of Directors. Meanwhile, the formal induction for new Directors also covers a range of essential training modules.

Additionally, the Board encourages knowledge sharing amongst the Directors. The Board being the highest governance body also acknowledges the importance of developing and enhancing its collective knowledge on economic, environmental and social topics. During the year 2024, the Directors attended the following training programmes focusing on both general aspects of directorship and matters specific to the industry.

- FATF Mutual Evaluation (ME) - India's Best Practice

- Awareness Session on Recent Amendments to the Listing Rules and a Reminder of Certain Laws which are being actively applied in Recent Times which Directors of Banks should be cognisant about

- Presentation on Sustainability and Value Creation (SLFRS S1 and S2)

- The Role of Governance in ESG and The Current Status of Sampath Bank

- ESG Summit 2024

- Directors' Duties in Information Security: Navigating Cybersecurity Risks in the Banking Sector

- Annual High-Level Awareness Conference for Licensed Banks, Licensed Finance Companies, Money or Value Transfer Service Providers and Primary Dealers in Sri Lanka (Topics -Strengthening Governance: Enhancing Board's Accountability in Financial Institutions for Effective Compliance against Money Laundering, Terrorist Financing and Proliferation Financing in Sri Lanka and Importance of Advanced Transaction Monitoring Systems for a Bank to Identify Suspicious Transactions)

- An Introduction to Embedding Sustainability/ ESG.

2.11 LEADERSHIP OF THE BOARD

Code 2023 Ref. - A.1.2

The Board recognises its duty to perform essential functions decisive to the Bank’s success. It plays a key role in guiding the Company with entrepreneurial leadership, establishing a solid framework of prudent and effective controls and managing risks, which are core to the governance structure. Furthermore, the Board's responsibilities have expanded across various spheres, requiring careful and vigilant monitoring to address emerging challenges and conquer opportunities, considering the scale, nature and complexity of the business.

2.12 FINANCIAL AND BUSINESS REPORTING

Code 2023 Ref. - D.1.2, D.1.4

The Board is responsible for ensuring that the Bank fulfils all its Financial Reporting obligations. Accordingly, it provides oversight to ensure that all regulatory reports are filed with relevant authorities in a timely manner, including but not limited to the Central Bank of Sri Lanka, the Department of Inland Revenue, the Registrar of Companies and the Colombo Stock Exchange. Interim Financial Statements reflecting quarterly results, as well as the Annual Report, are published within the timelines stipulated by relevant regulatory authorities, enabling shareholders to understand the state of affairs of the Bank.

The Annual Report of the Board of Directors on the Affairs of the Company provided on pages 255 to 263 includes the declarations required by the Code 2023 concerning of financial and business reporting.

2.13 COMPLIANCE WITH CAPITAL ADEQUACY REQUIREMENTS

Direction 2024 Ref. - 1.10

Direction 2007 Ref. - 3(1)(xv)

The Board monitors capital adequacy and other prudential measures as necessary to ensure that the Bank is capitalised at levels required by the CBSL from time to time. Additionally, the Bank has established a defined risk appetite and considers industry benchmarks when evaluating capital adequacy requirements. During the year under review, the Bank complied with the minimum capital adequacy requirements. To mitigate risks arising from macroeconomic challenges, the Bank has maintained an internal capital buffer above the minimum requirements set by the regulator.

2.14 ESTABLISHMENT AND MAINTENANCE OF POLICIES IN TERMS OF LISTING RULES AND CODE 2023

Listing Rule Ref. - 9.2.1, 9.2.3, 9.2.4, 9.5.1, 9.5.2, 9.10.1

Code 2023 Ref. - I.1, I.1.1, I.1.3, I.1.4, I.2, I.2.1, I.2.2

The Bank in compliance with the Listing Rules and the Code 2023 established following policies and made available the same in the Bank's Corporate Web www.sampath.lk with effect from 1st October 2024. The policies are available for the shareholders, upon submission of a written request to the Company Secretary.

- Policy on Matters Relating to the Board of Directors

- Policy on Board Committees

- Policy on Corporate Governance

- Policy on Nominations and Re-election of Directors

- Policy on Remuneration

- Policy on Internal Code of Business Conduct and Ethics for Directors

- Policy on Internal Code of Business Conduct and Ethics for Employees

- Policy on Risk Management and Internal Controls

- Policy on Relations with Shareholders and Investors

- Policy on Environmental, Social and Governance Sustainability

- Policy on Control and Management of Bank Assets and Shareholder Investments

- Policy on Corporate Disclosures

- Policy on Whistleblowing

- Policy on Anti-Bribery and Corruption

Consequent to the publication effective from 1st October 2024, no amendments have been made to the aforementioned list of

policies, except for the amendment made to the "Policy on Whistleblowing", "Policy on Matters Relating to the Board of Directors"

and "Policy on Internal Code of Business Conduct and Ethics for Directors" as mentioned below:

Following the regulatory requirements specified in the Direction 2024 the Board undertook necessary steps to amend the said

Policies as mentioned below.

- "Policy on Whistleblowing” on 31st December 2024 by incorporating regulatory requirements under heading “3. Reporting mechanism”.

- "Policy on Matters Relating to the Board of Directors" on 14th February 2025 by incorporating regulatory requirements under headings "1. Board Composition, 2. Board Responsibilities, 3. Obligations, 4. Board Meetings, 5. Chairperson, 6. Managing Director (MD), 7. Appraisal of the Board and MD and 8. Training".

- "Policy on Internal Code of Business Conduct and Ethics for Directors" on 14th February 2025 by incorporating regulatory requirements under headings "1. Standard of Conduct, 2. Key Responsibilities, 3. Fitness and propriety, 4. Conflicts of Interest, 5. Confidentiality, 6. Dealing with Financial and Non-Financial Benefits and Gifts, 7. Accommodation Granted to Directors and Connected Parties, 10. Fair Treatment to Customers, 11. Integrity in Reporting, 12. Corporate Opportunities, 13. Protection and Proper Use of Bank Assets Including Information Assets and 15. Training".

2.15 CODE OF CONDUCT AND ETHICS

Direction 2024 Ref. - 1.1(s), 1.1(t)

Listing Rule Ref. - 9.2.2

Code 2023 Ref. - D.6, D.6.1, D.6.3, D.6.5, D.6.6, D.6.7, I.1.2

The Board collectively and Directors individually set the tone from the top for promulgating the culture of ethics and integrity across the Bank. In this regard, the "Policy on Internal Code of Business Conduct and Ethics for Directors", the Code of Conduct for Corporate Management and the Code of Conduct for other Employees are in place to ensure good governance and to inculcate a sound corporate culture that reinforces norms for professional, ethical and prudent behaviour throughout the Bank. These guidelines are reviewed periodically and updated in keeping with the latest developments. Moreover, it addresses the issues on confidentiality of data, conflicts of interest, procedures for dealing with financial and non-financial benefits and gifts, integrity in reporting and the fair treatment to customers. Bank-wide internal guidelines and the "Policy on Anti-Bribery and Corruption" have also been implemented to intensify the Bank's commitment towards anti-corruption practices.

The Bank has conducted internal training related to the code of business conduct and ethics as part of induction programmes for new employees and has obtained confirmation of compliance from all employees.

A process is in place to monitor the share transactions carried out by the Directors, KMPs and identified employees involved in financial reporting in a timely manner.

The Chairman's affirmation with regard to introduction of a Bank-wide Code of Conduct and Ethics, the status of compliance with same and his awareness of any violations thereof are given on page 148 of this Annual Report.

3) RELATIONSHIPS AMONG THE DIRECTORS INCLUDING THE CHAIRMAN AND MANAGING DIRECTOR

Direction 2024 Ref. - 1.2, 5, 5.1, 9.2(h)(iii)

Direction 2007 Ref. - 3(1)(ii), 3(5)(i), 3(5)(iii)

Listing Rule Ref. - 9.6.1, 9.6.2

Code 2023 Ref. - A.2, A.2.1

The Board has duly appointed the Chairman and the MD of the Bank and their functions and responsibilities are defined in line with the regulatory requirements. In that respect, the functional responsibilities of the Board Chairman and the MD are clearly documented and duly approved by the Board. The Chairman is a Non-Executive Director whilst the MD serves as an Executive Director. The identity of the Chairman and MD are disclosed in the Annual Report on page 186. There is no material financial, business or family relationships between the Chairman, MD and other members of the Board as disclosed on pages 262 and 263, and in Note 47 to the Financial Statements given on pages 363 to 366. The above disclosures are made as per the annual declarations and the Register of Directors' Interests which are updated regularly.

3.1 THE CHAIRMAN

Direction 2024 Ref. - 5.2(b), 5.2(c), 5.3(a), 5.3(b), 5.3(c), 5.3(d), 5.3(e), 5.3(f), 5.3(g), 5.3(h), 5.3(i)

Direction 2007 Ref. - 3(5)(iv), 3(5)(v), 3(5)(vi), 3(5)(vii), 3(5)(viii), 3(5)(ix), 3(5)(x)

Code 2023 Ref. - A.3, A.3.1, A.5.9

The Chairman leads the Board ensuring that it functions and duly discharges its responsibilities effectively while all key and appropriate issues are discussed by the Board in a timely manner.

The Chairman ensures that the "Policy on Internal Code of Business Conduct and Ethics for Directors" and the Terms of Reference (TOR) of Board and each Board Sub-Committee spells out the Directors’ duties and responsibilities and the standards of care expected from them. The Chairman further ensures that Directors are properly briefed on issues arising at Board Meetings and also ensures that Directors receive adequate information in a timely manner.

The Board Chairman is responsible for ensuring the right mix between EDs and NEDs to ensure an appropriate balance of power to support independent and objective decision making at Board level. Further, the Chairman facilitates the effective contribution of NEDs in particular and ensures constructive discussions between EDs and NEDs.

The Chairman, in consultation with all other Directors and the Company Secretary, develops the routine agenda for Board Meetings, ensuring that all important areas for discussion are covered. Additionally, he encourages full and active participation of both EDs and NEDs at Board meetings, facilitates the expression and discussion of dissenting views and fosters proactive involvement in the Bank's best interests. The same is evident from the responses in the self-evaluation forms submitted by each Director at the end of the year. During the year under review, the Chairman held two (02) meetings on 26th July 2024 and 30th November 2024 with NEDs without the EDs being present as per the governance requirements.

The Chairman ensures that the Board has the oversight in respect of the Bank’s affairs and its obligations to its depositors, shareholders

and stakeholders as appropriate whereas he does not engage in activities involving direct supervision of any employee or partake in

any other executive duties whatsoever. The Chairman of the Board who is also a member of BSRC ensures that appropriate steps

are taken to maintain effective communication with shareholders and that the views of shareholders are communicated to the Board.

The Board taking into consideration the requirements stipulated under Section 5.2 of the Direction 2024, will make necessary

arrangements to comply with the same.

3.2 THE SENIOR INDEPENDENT DIRECTOR

Direction 2024 Ref. - 5.2(a)

Direction 2007 Ref. - 3(5)(ii)

Listing Rule Ref. - 9.6.3(a), 9.6.3(b), 9.6.3(c), 9.6.3(d), 9.6.3(e), 9.6.4, 9.10.4(i)

Code 2023 Ref. - A.1.2, A.5.7, A.5.8

The Board has appointed Mr Dilip de S Wijeyeratne as the Senior Independent Director (SID) of the Board considering the fact that the Chairman is a Non-Independent Director. The position of SID is governed under the Board approved TOR which is in place with the intention of ensuring a greater independent element. The profile of the SID is given on page 187 of the Annual Report. The “Report by the Senior Independent Director” is given on page 195, demonstrating the effectiveness of his duties.

During the year under review, the SID conducted meetings fulfilling regulatory and best practice requirements and the details of such

meetings are given in the “Report by the Senior Independent Director”.

In line with the Board approved TOR for the SID, the SID holds a casting vote at aforementioned meetings and provides his feedback

and recommendations from such meetings to the Chairman and other Board members as appropriate. The SID is also available for

confidential discussions with other Directors and represents all shareholders at meetings.

3.3 THE MANAGING DIRECTOR

Direction 2024 Ref. - 5.4, 5.5

Direction 2007 Ref. - 3(5)(xi)

The MD, as the apex senior executive, is accountable to the Board for leading the Corporate Management Team and managing the Bank's day-to-day operations and business. The MD ensures the implementation of Board-approved policies and that the Bank meets its regulatory and fiduciary commitments.

The MD has been appointed as a NED of Sampath Centre Limited which is a fully owned subsidiary of the Bank. In addition to the above, the MD has also been appointed as a Director in other institutions established for the development and effective functioning of the banking industry. The profile of the MD is given on page 186. Despite these additional roles, the MD ensures such directorships do not hinder her ability to devote sufficient professional time to discharge her duties as the MD of the Bank. Further, the MD has fulfilled the Fit and Proper Assessment Criteria outlined in Section 44A and Section 76H of the Banking Act and possesses sufficient authority, stature, knowledge, competencies and expertise in the core banking functions given the size, scale, diversity and complexity of operations of the Bank.

4) MANAGEMENT FUNCTIONS DELEGATED BY THE BOARD

Direction 2024 Ref. - 4, 4.1, 4.3, 4.4

Direction 2007 Ref. - 3(4)(i), 3(4)(ii), 3(4)(iii)

Code 2023 Ref. - A.1.2

The Board clearly understands the delegation arrangements in place and consciously delegates authority to the Management to carry out certain duties to ensure a greater balance of power and authority so that powers are not concentrated in any individual. Such delegation does not hinder the Board's ability to discharge its functions within the provisions of the Bank's Memorandum and Articles of Association. The Management, who carries out duties on behalf of the Board under such delegated authority are required to report to the Board regularly on such matters attended by them.

The Board reviews and approves delegation arrangements as and when required, ensuring they address the Bank's requirements while allowing the Board to function effectively. The following Operational Level Committees offer more specialised supervision over functions that are delegated by the Board.

| Management Committees | ||

|---|---|---|

| Advances Committee | Executive Advances Committee | Operational Risk Management Committee |

| Asset & Liability Management Committee (ALCO) | Fraud Risk Management Committee | Outsourcing Committee |

| Corporate Management Committee | Information Security Committee | Procurement Committee |

| Credit Policy, Risk and Portfolio Review Committee | Internal Capital Adequacy Assessment Process (ICAAP) Working Committee | Recovery Plan (RCP) Working Committee |

| Data Dissemination Committee | Internal Control Over Financial Reporting (ICOFR) Committee | Risk and Compliance Committee |

| Disciplinary Committee | Investment Committee | Transfer Committee |

| Dissemination of Regulatory Instructions Committee | IT Steering Committee | Vision 2028: Steering Committee |

| Environmental, Social and Governance Committee | Model Risk Management Committee | |

5) CYBER SECURITY AND INTEGRITY OF INFORMATION

Code 2023 Ref. - A.1.2, G.1, G.2, G.3, G.4, G.5

Operating under the delegated authority of the Board, the Board IT Committee (BITC) provides oversight for the implementation of the Bank IT strategy, vis-à-vis digital product innovation and ensuring the robustness of the Bank’s IT infrastructure to support overall strategic objectives and risk management targets. The BITC provides oversight to address IT related matters of the customers and the employees while recommending the IT strategic plan, policies, expenditure and budgets to the Board. The BITC ensures that the Bank continuously invests in advanced security controls to detect and respond to the latest threats effectively.

Considering the rapidly evolving nature of the modern technology world, the Board has allocated sufficient time during each Board Meeting to allow the BITC to present their views on the risk factors that may have a bearing on the IT needs including cyber risk management of the Bank. Further, the Directors are concerned with the manner in which the challenging economic state of the country and the complexity of expanding digital operations have negatively impacted the number of financial crimes that were being recorded. During the year under review, the Board participated in Cyber Security Awareness session conducted by an industry professional.

With the goal of maintaining the integrity and confidentiality of the data handled by the Bank, the Information Security Committee (ISC) was established to oversee the strategic and operational aspects of information security within the Bank. The ISC apprises the BIRMC on a quarterly basis on the matters that were being highlighted during the period.

The Information Security Department (ISD) headed by the Chief Information Security Officer (CISO) is tasked with determining the Bank's sensitivity and risk appetite towards information security threats at any given time. Towards ensuring the Bank's cyber security controls, the Bank has aligned with the global best practices by obtaining the ISO 27001 standards certification to validate the efficacy of the Bank's Information Security Architecture. The ISD monitors privilege access using the latest Privilege Access Management (PAM) software. The annual Risk Assessments are conducted covering all departments and the selected branches to identify potential information security risks and formulate appropriate risk treatment plans. Meanwhile, a cross functional incident response team was appointed and granted authority for taking immediate actions in the event of an information security breach to ensure business continuity and information security. A cross functional management committee (Data Dissemination Committee - DDC) was formed to manage and evaluate the information shared by the Bank internally and externally. Moreover, the Bank has implemented Data Loss Prevention (DLP) solution to manage/restrict information shared by the Bank internally and externally. To ensure the information security of the payment cards, the Bank has recently obtained PCI: DSS V3.2.1 Certification. Further, it will comply with terms of payment brands and ensure security of payment cards. To ensure the security of customer's digital experience, ISD continuously monitors external threats such as phishing attacks, bogus web contents and applications with an association of external service provider. In addition to that ISD provides customer awareness in information security frequently and where necessary. Additionally, the Bank has obtained cyber security insurance cover to enhance its information security measures.

The Bank has implemented multiple firewalls and other systems to secure its internal systems. In addition, the Bank's ISD reviews routine Vulnerability Assessments and Code Reviews to test the efficiency and integrity of these information systems in safeguarding against external and internal breaches.

All devices connected or attached to the Bank's infrastructure are authorised by a Network Access Controller and the use of other remote access solutions is strictly prohibited unless otherwise written approval has been obtained. Remote access is granted to users outside of the Bank with a justifiable business requirement, while access points into the Bank's ecosystem are regularly assessed with any changes that are formally approved.

The Bank also obtains the services of an external specialist to conduct quarterly Vulnerability Assessments and Annual Penetration Tests to identify vulnerabilities and determine possible threats in order to initiate necessary preventive actions. In addition, the Bank conducts periodic Cyber Security Drills to promote information security awareness among the staff members and a Bank-wide Information Security Risk Assessment Review was conducted in 2024 with the support of an independent expert entity.

The relevant disclosure of the process to identify and manage cyber security risk is given on pages 246 to 248 in this Annual Report.

6) SUSTAINABLE DEVELOPMENT AND ESG (ENVIRONMENTAL, SOCIAL AND GOVERNANCE)

Direction 2024 Ref. - 1.1(w)

Code 2023 Ref. - A.1.2, H.1, H.1.1, H.2, H.2.1, H.3, H.3.1, H.4, H.4.1, H.4.2, H.4.3, H.5, H.5.1, H.5.2, H.5.3, H.5.4

The Board, when considering business sustainability, focuses on integrating Environmental, Social and Governance (ESG) factors into decision making processes. Key considerations include aligning sustainability with the Bank's strategy, managing risks and opportunities related to ESG issues, engaging with stakeholders, ensuring compliance with regulations and ethical standards, fostering innovation for sustainable practices, promoting social responsibility and enhancing investor relations by demonstrating a commitment to sustainable business practices. By addressing these aspects, the Board seeks to foster responsible and ethical operations to build resilience, while contributing positively to societal and environmental progress. The Bank is conscious of its role in addressing various environmental implications and driving towards sustainable socio-economic developments. The Bank has initiated various projects for the purpose of protecting the environment and biodiversity, restoration of natural resources and sustainable use of resources.

As a result of prioritising the ESG within the Bank, the Board has established a Board Sub-Committee to address the risks and opportunities pertaining to the business operation and promote the ESG considerations. The Board Sustainability Committee (BSC) was established on 29th May 2024 by the Board of Directors also to comply with the requirements of paragraphs 26 and 27 of SLFRS S1: General Requirements for Disclosure of Sustainability-related Financial Information. The Committee consists of four (04) Independent, NEDs and the MD. The Bank established the BSC with the primary objective of overseeing the development and implementation of the Bank's sustainability strategy and policies and specifically addressing the sustainability related risks and opportunities. The Board Sustainability Committee Report is given on pages 210 and 211.

Further, the Bank has established an ESG working group with members from all departments and branches to drive the ESG strategic priorities. All the “ESG Champions” from the departments and branches have been appointed during the year under review and the said individuals will be trained to implement the environmental management system to conserve the environmental aspects.

Each employee holds a key task to contribute towards the ESG strategy. Additionally, ESG Management Committee has been

formed to develop/enhance the Bank's ESG/sustainability strategy and policies, decision making, defining/redefining materiality for

sustainability related risks and opportunities including climate related physical risks and transition risks, responding to sustainability

related risks and opportunities, integration of ESG/sustainability matters, direction to business units, establishment of targets, skills

and competencies development, improvement of ESG/sustainability disclosures and performance, escalation mechanisms, report

to BSC, on recommendations on ESG Trends, Green Sustainable Lending, Green Borrowings and Sustainability Reporting. The

Committee meets on a monthly basis or as and when required. The TOR of the ESG Management Committee has been developed

mapping the key contribution from the KMPs towards the successful ESG implementation and continuation.

The key pillars managed by the ESG Management Committee, which contribute to the overall ESG strategies of the Bank, along with

the Committee Chair are, governance, investment decisions, green products such as (Green/Sustainable) borrowings/lending, CBSL's

roadmap for Sustainable Finance in Sri Lanka, ESG commitments in the Direction 2024, the Code 2023, ESG Risk Management,

Corporate Social Responsibility (CSR) Programmes and ESG Communications.

The Board has always strongly emphasised strengthening the Bank's ESG credentials. The Bank has implemented an Environmental and Social Risk Management System (ESMS) to manage the environmental and social risks associated with the Bank's credit operation, thereby reducing the Bank's environmental footprint and improving its social well-being. The ESMS Implementation Committee was formed and a dedicated ESMS Officer was appointed to further strengthen the ESMS by implementing a suitable Environmental and Social Risk Management Framework to identify and measure environmental and social risks at all levels of operations across the Bank. The Bank issued the ESG Policy and CSR Policy to further strengthen the ESMS in the Bank. Additionally, all employees are encouraged to adopt the Environmental Pledge, while regular training and awareness building initiatives to ensure staff have adequate knowledge to understand the purpose, application and intended objectives of the ESMS. In this regard, staff capacity building on environmental and social due diligence is conducted by the Corporate Learning Centre on a periodic basis in collaboration with the Corporate Sustainability Department.

The adoption of integrated reporting is a key focus, combining financial and non-financial data to offer a transparent and holistic view of the Bank's performance. This approach not only enhances accountability but also meets stakeholders' expectations for responsible business practices. The Board meticulously has taken steps to evaluate ESG risks and opportunities, embedding these factors into the Bank's operations to foster resilience and sustainable growth. Upholding the highest standards of corporate governance, the Board ensures that all actions contribute to long-term value creation and effective risk mitigation. This comprehensive approach underscores the Bank's dedication to sustainability and responsible banking.

The Board and Board Sub-Committees, with a view to identifying and managing the social, economic, and environmental topics and their impacts, may from time to time call for comprehensive analysis reports from both external and internal resource personnel to be in line with the adequate due diligence. Further, the Board reviews the ESG factors where necessary to enhance the ESG-related areas. Moreover, information pertaining to CSR initiatives and sustainability framework of the Bank is given on the following reports.

- Our Approach to Sustainability is given on pages 33 to 38.

- Natural Capital Report is given on pages 110 to 128.

- Social and Relationship Capital Report is given on pages 94 to 109.

- Material Topics is given on pages 46 to 48.

7) BOARD APPOINTED COMMITTEES

Direction 2024 Ref. - 6, 6.1, 9.2(g)

Direction 2007 Ref. - 3(6)(i)

Listing Rule Ref. - 9.3.1, 9.3.2, 9.3.3