Management Discussion And Analysis

Business Reports

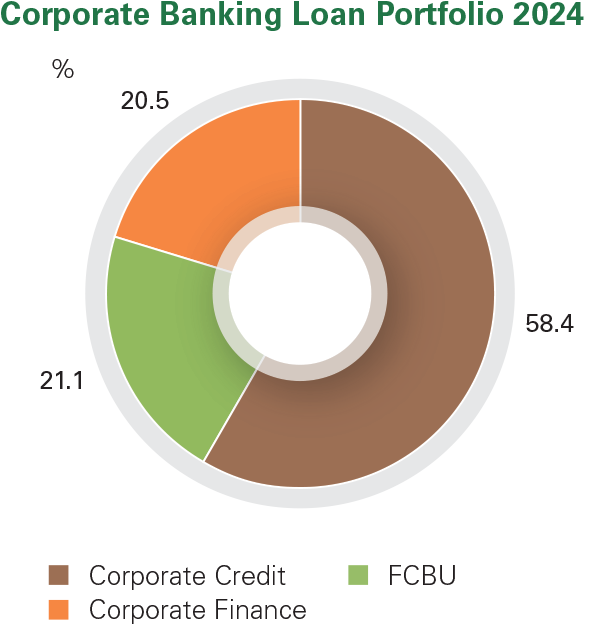

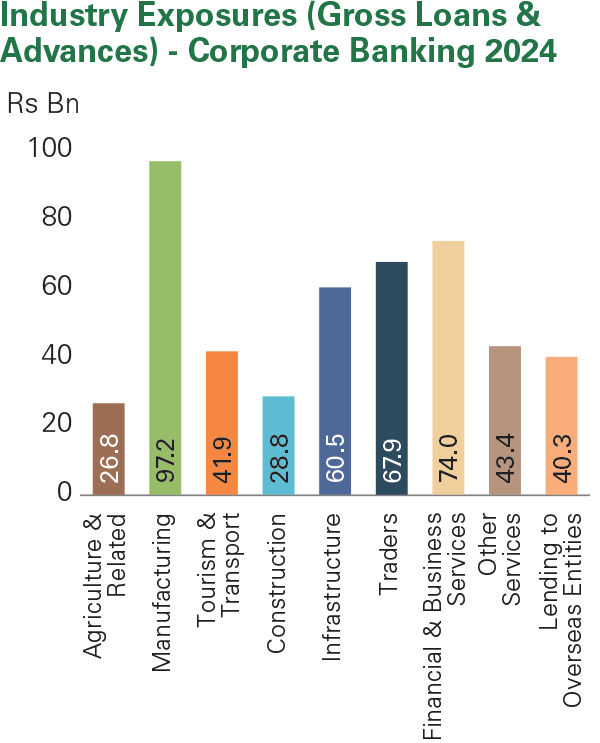

Corporate Banking comprises Corporate Credit, Corporate Finance, FCBU and International Trade Departments of the Bank. Collectively, these four departments support growth of the country’s corporate sector, leveraging its highly specialised skills to customise solutions for large enterprises.

Rs 16 Bn

Segment Operating Profit 2024 (before tax)

Rs 442 Bn

Segment Assets 2024

Rs 428 Bn

Segment Liabilities 2024

Our Services

- Export Financing

- Import Financing

- Warehouse Financing

- Dealer Financing

- Cash Management

- Business Loans

- Investment Banking

- Syndicated Loans

- Custodian Services

- Infrastructure Investment including Renewable Energy

- Escrow Facilities

- Margin Trading

- Financial Sector Financing

- Offshore Lending

- Export Sector Financing

- Managing Corporate FCBU Accounts

- Establishment of Documentary Credits (DC)

- Arranging Confirmation for DCs

- Issuance of Shipping Guarantees

- Purchasing/Negotiation of DCs and Collection Bills

- Inward Remittances

- Outward Remittances

- Overseas Student Payments

Market Review

2024 witnessed economic stability although forecast elections dampened investment appetite. Earnings of corporates reflected the pressures on discretionary income as consumption remained at a low ebb. Interest rates declined by 228 bps in 2024 after a sharp decline of 449 bps in 2023, significantly impacting NII for the second consecutive year. CBSL also tightened regulations regarding lending, impacting the growth of the corporate loan book. The return to stability and lower interest rates contributed to improved cash flows, supporting recovery. However, activity in the Colombo bourse was mellow, dampening issuer and investor sentiments alike resulting in low levels of activity.

The growth momentum of the Tourism sector was encouraging, contributing to dollar liquidity in the market. Exporters also experienced positive growth during the year boosted by the routing of orders from Bangladesh in the aftermath of the country’s economic struggles. Imports also increased during the year. We also witnessed a gradual uptick in the construction sector, particularly in housing and condominiums. The government’s stated target of having 70% of the country’s energy requirement generated through renewable energy provided momentum for growth in the renewable energy sector of the Corporate Finance portfolio.

Economic instability in South Asia was a concern during the year while the strong growth trajectory of India presented an opportunity for growth for offshore banking.

Strategy

Delivering Results in 2024

| Performance Highlights | |||

|---|---|---|---|

| 2024 Rs Mn |

2023 Rs Mn |

Change % |

|

| Net interest income | 15,926 | 31,725 | (49.8) |

| Net fee & commission income | 4,785 | 5,838 | (18.0) |

| Net other operating income | 105 | 116 | (9.8) |

| Inter-segment expenses | (414) | (959) | 56.8 |

| Total operating income | 20,402 | 36,720 | (44.4) |

| Less: Impairment charge | 3,335 | 8,546 | (61.0) |

| Net operating income | 17,067 | 28,174 | (39.4) |

| Less: Total operating expenses | 860 | 769 | 11.9 |

| Operating profit before tax | 16,206 | 27,405 | (40.9) |

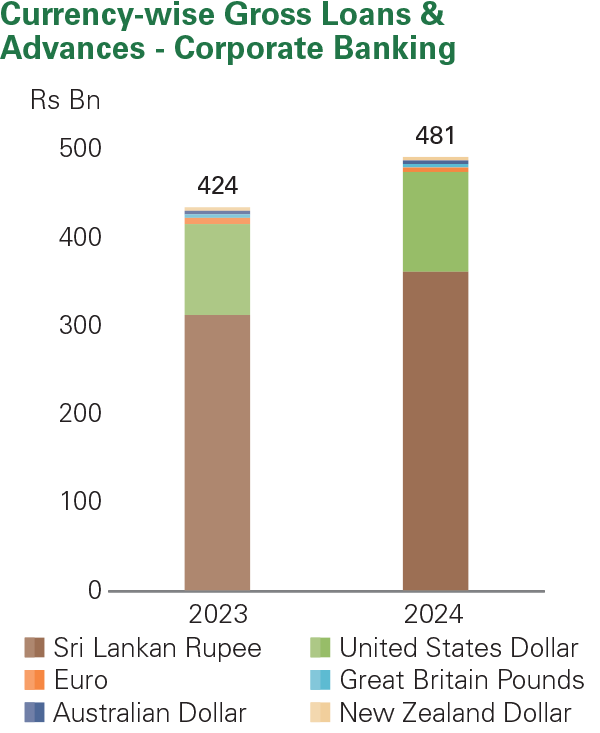

| Segment assets | 442,436 | 399,964 | 10.6 |

| Segment liabilities | 428,355 | 375,296 | 14.1 |

Note: The segment assets, liabilities, income, and expenses figures mentioned above include inter-segment balances.

61%

Rs 3.3 Bn

Impairment Charge

2023: Rs 8.5 Bn

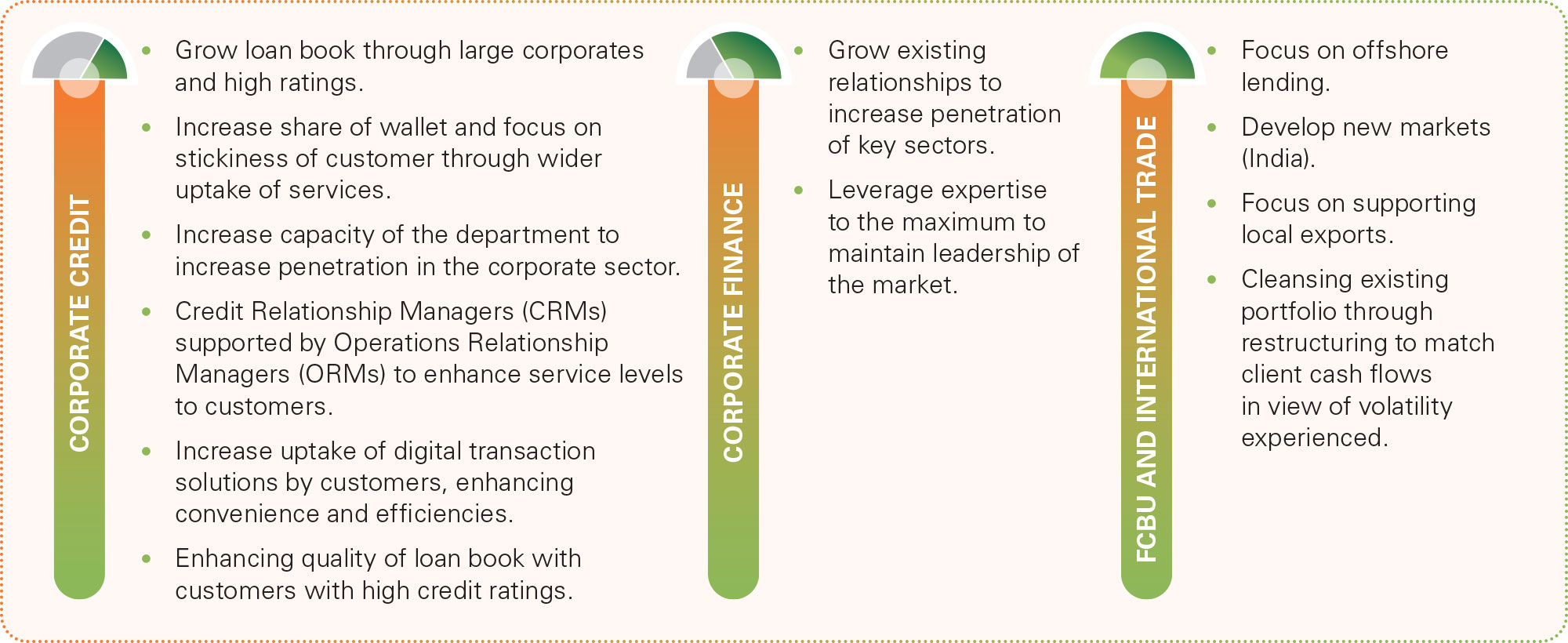

CORPORATE CREDIT

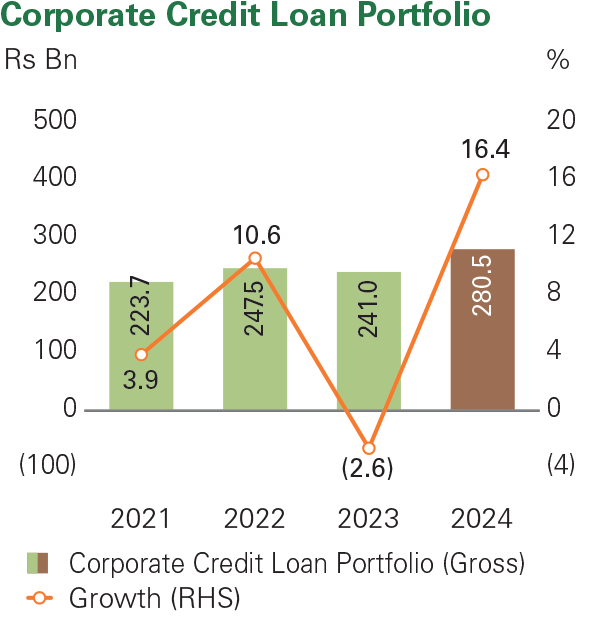

Corporate Credit recorded a stable year recording portfolio growth of 16.4%. Continued focus on large, resilient corporates and resurging sectors contributed to the improvement in credit quality of the portfolio as evinced by the decrease in stage II and III portfolio balances. Recoveries improved supported by recovery and growth in some sectors. Corporate Credit also restructured facilities where deemed necessary to match customer cash flows with repayments, facilitating recovery.

With the strategies introduced by globally renowned consultants, new positions were created to ease the operational workload of the Customer Relationship Managers and allow them to focus more on driving credit growth and transaction banking volumes through improved data analytics to formulate client specific strategies. Sustainable financing was a key focus with the institutionalising of ESMS prior to approval to ensure that environmental and social impacts of projects financed are considered in the approval process. This has paved the way for the Bank to steer its clients towards adopting socially and environmentally compliant business practices.

CORPORATE FINANCE

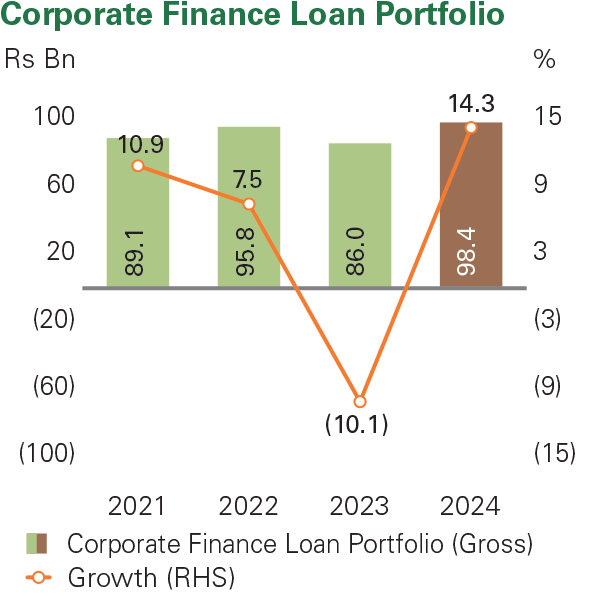

Activity in Corporate Finance was driven by strong interest in renewable power generation project financing. The Bank’s specialised technical knowledge and support throughout the process continues to provide a strong competitive edge in an increasingly competitive market. Consequently, the Bank continued to enjoy strong pipelines, a necessity given the long gestation period of infrastructure projects. However, both NIM and NII declined during the year with the decline in interest rates which corrected with macro stability, dampening earnings. However, fee based income increased during the year due to strong cross selling of the Bank’s services during the year.

FCBU

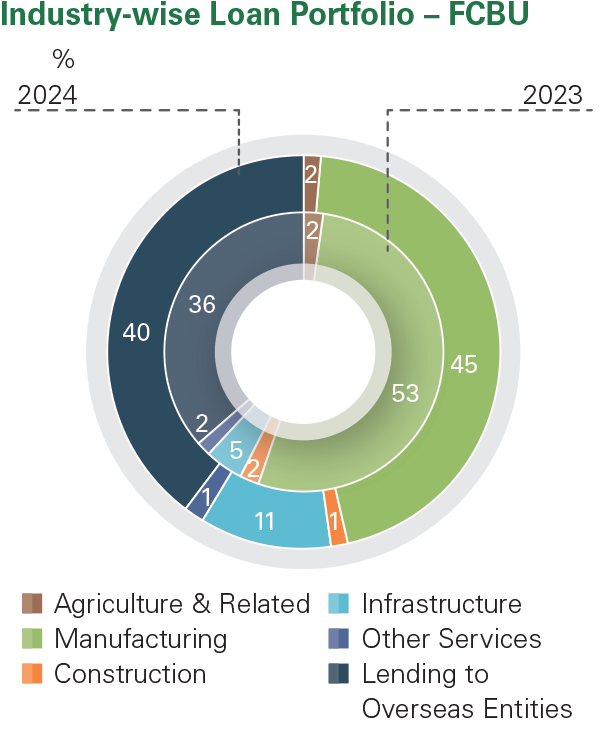

The offshore lending unit of the Bank recorded positive portfolio growth of 5.4% supported by growth in apparel, port and infrastructure development, overseas institutional lending and Agri export sectors. Client relationships were strengthened with regular interactions which strengthened information flows enhancing monitoring and identification of early warning signs amidst significant uncertainty and potential downside risks. The entry into India was a positive step to capitalise on the opportunities presented by India’s ascent as the 5th largest economy in the world. Impairment charges increased due to exposures to the vulnerable sectors which are being monitored closely. The strategy of growth with established clients has supported credit quality and management of cross-border risk. The unit is keen to institutionalise sustainable financing and is looking to widen the scope of this opportunity.

Following the enactment of the Banking (Amendment) Act No. 24 of 2024, the segregation between the Domestic Banking Unit (DBU) and the Offshore Banking Unit (OBU) has been removed. Offshore banking activities are now recognised as permissible operations for Licensed Commercial Banks (LCBs). Despite this regulatory change, the Bank continues to operate its Foreign Currency Banking Unit (FCBU) as a separate unit under its business model, ensuring the delivery of seamless services to customers.

INTERNATIONAL TRADE

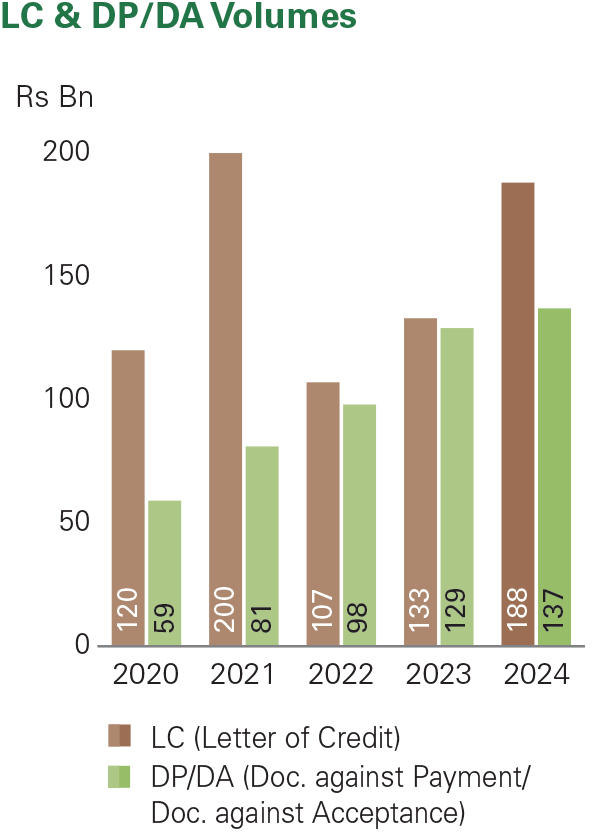

Increased import and export volumes and increased liquidity in foreign exchange supported increased activity in international trade business. However, this led to intense competition, exerting pressure on fees and interest rate spreads. Despite this, the Bank was able to increase its market share of exports from 9% to 12% and imports from 8% to 10%, a noteworthy achievement underpinned by successful implementation of strategy. Increased focus on customer centricity and service excellence supported increased shares of customer wallets as well as acquisition of new clients. As the country situation improved, the Bank was also able to increase its network of correspondent banks to enhance service levels to customers.

The Bank also strengthened its position in foreign currency remittances for students with its focus on customer centricity and the sponsorship of two major education fairs and other targeted initiatives. Accordingly, this area of business recorded 30% growth over the previous year.

The Bank has identified the importance of building the capacity of potential regional SMEs to help them become exporters. To support this objective, the Bank collaborated with the Export Development Board of Sri Lanka in their regional awareness sessions for SMEs registered under the New Exporter Development Programme. This partnership aims to bridge the knowledge gap for these entities regarding export market entry requirements.

Imports

2%

share from 8% to 10%

share from 8% to 10%

Exports

3%

share from 9% to 12%

Student Remittances

30%

42

Nostro Accounts

532

Correspondent Banks

97

Exchange Companies

Scan this QR code for a comprehensive view of our Nostro Accounts, Correspondent Banks and Exchange Companies

- Market stability is expected to prevail in Sri Lanka although there may be a correction in the interest rates and exchange rates with a slight upward movement in both. As credit growth gathers momentum with policy stability, competition in corporate banking is likely to remain at elevated levels in growth sectors and large corporates. Increased trade volumes and customer focus on convenient digitalised services are expected to support growth in fee based income. Importantly, initiatives launched with regards to capacity building within our teams during the year are expected to strengthen relationships, supporting growth and market positioning in this key segment.

- Higher levels of economic activity are also expected to benefit Corporate Finance and stability is expected to attract foreign investor interest as well. GOSL plans for infrastructure development will need private sector participation which augurs well for portfolio growth. Sampath Bank’s leadership position in renewable energy and its value added offering supports its aspirations for growth in this defensive sector. Financial services companies are also expected to expand their activities, further stimulating growth.

- FCBU activity will be buoyed by export growth as uncertainties ease, increasing opportunities for growth amidst continuing turmoil in South Asia. We also expect to grow the offshore book in India as customers move into this high growth economy with continuous monitoring of geopolitical and socioeconomic developments in adjacent countries. Trade volumes will be key to growth together with stability in the country as Sri Lanka seeks to position itself as a stable manufacturing location.

- In the short term, the country’s recovery and the uncertain political landscape is likely to temper growth rates and significant uncertainty prevails over potential disruptions to global supply chains. Upside potential includes strengthening of bilateral trade through trade agreements and a renewed focus on import of essential items. Policy reforms and debt restructuring are key to medium and long term stability while exporters may face challenges to global markets through both tariff and non-tariff measures such as ESG requirements. Diversification of exports and increased value addition is key to growth in the medium to long term as well as sustained growth of the tourism sector to ensure liquidity in foreign exchange markets.