Management Discussion And Analysis

Operating Environment

|

|

|---|---|

|

Impact on Sampath Bank and Our ResponseGiven the uncertainty that prevailed, the private sector adopted a cautious approach to investment, softening credit demand. In view of this, the Bank sought alternative investment options for surplus funds including investments in US Treasuries. |

|

|

|---|---|

Significant Milestones Strengthen the Nation’s Economic Stability....Successful Completion of Sri Lanka’s External Bond Restructuring Programme

Ongoing Commitment to the IMF Extended Fund Facility Programme

Sovereign Credit Rating Upgrade

X Gross Domestic Product (GDP)

|

|

Interest Rate Movement

An accommodative monetary policy stance resulted in the continued decline in interest rates. Inflation

Inflation maintained a downward trajectory, with headline inflation standing at -1.7% in December 2024. Exchange Rate Movement

The Sri Lankan Rupee appreciated by 10% against the USD to Rs 292.58 during 2024 supported by enhanced inflows from workers’ remittances, tourist earnings and export conversions. |

|

Tourism Sector Revival

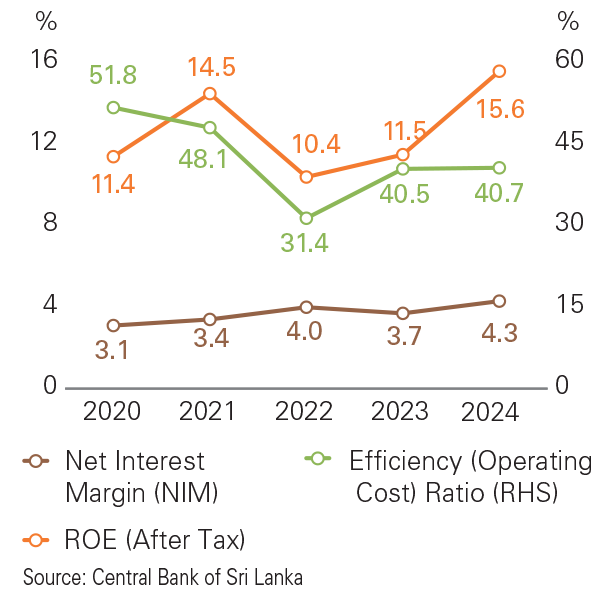

The tourism sector continued to show signs of recovery with earnings expanding by 53.2% to USD 3.2 Bn as at end-December 2024. Worker RemittancesWorker remittances maintained its upward trajectory expanding by 10.1% to USD 6.6 Bn as at end- December 2024. Impact on Sampath Bank and Our ResponseWe proactively capitalised on opportunities that emerged from the gradual economic recovery, tailoring our strategy to facilitate business revival in economically significant sectors, including tourism, agriculture, renewable energy, healthcare and trade. Specific emphasis was placed on supporting and building resilience within the SME sector, through customised lending, expert advice and guidance to improve business operations and strategic planning through the expertise of the Business Revival Unit. The Bank also focused on strengthening its market position in the remittance market. Furthermore, the Bank accepted the local bonds option in the GOSL’s ISB restructuring, converting 30% of the dues into Sri Lankan Rupee bonds and accepting new USD bonds for the remainder which was subject to a 10% haircut. Accordingly, impairment charges of Rs 15.8 Bn recognised for the ISBs were reversed. Overall, our strategic efforts contributed to a 59.4% increase in PAT and a ROE of 17.74% which stood among the best in the industry. |

|

Significant Milestones Strengthen the Nation’s Economic Stability....

Successful Completion of Sri Lanka’s External Bond Restructuring Programme

- Following two years of intense negotiations, Sri Lanka successfully concluded its International Sovereign Bond (ISB) restructuring in December 2024, with a significant majority of investors exchanging their existing bonds for new debt instruments. The agreement resulted in the restructuring of approximately 96% of the nation’s total commercial external debt amounting to USD 12.6 Bn.

- The nation also reached an agreement in principle with most commercial creditors including international banks for a further USD 200 Mn, with the restructuring due to be completed by the year-end.

- The international debt restructuring is expected to alleviate the country’s debt burden considerably, enabling the re-direction of resources towards vital development initiatives and social welfare programmes while establishing a sound foundation for long-term fiscal stability.

Ongoing Commitment to the IMF Extended Fund Facility Programme

- Sri Lanka reached a staff-level agreement with the IMF on the third review under the Extended Fund Facility Arrangement, granting the country access to approximately USD 333 Mn in financing.

Sovereign Credit Rating Upgrade

- Following the conclusion of the ISB restructuring and an improved outlook for the country’s macro- economic indicators, Fitch Ratings and Moody’s Ratings upgraded Sri Lanka’s long-term foreign currency issuer rating to CCC+ and Caa1 (stable outlook) respectively. Fitch Ratings also upgraded the nation’s local-currency issuer rating to CCC+ from CCC- to align with the upgrade in the long-term foreign currency issuer rating.

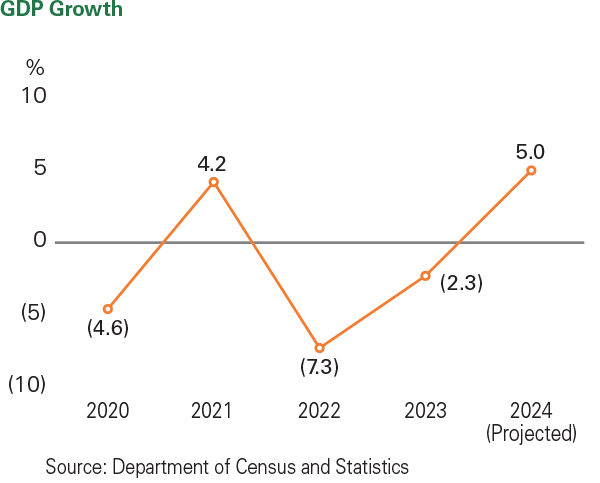

Gross Domestic Product (GDP)

- The Sri Lankan economy continued to demonstrate recovery with GDP expanding by 5% (projected) during 2024.

- All major sectors recorded positive growth with Agriculture, Industry and Services expanding by 1.9%, 11.2% and 2.6% respectively up to Q3 2024.

Interest Rate Movement

An accommodative monetary policy stance resulted in the continued decline in interest rates.

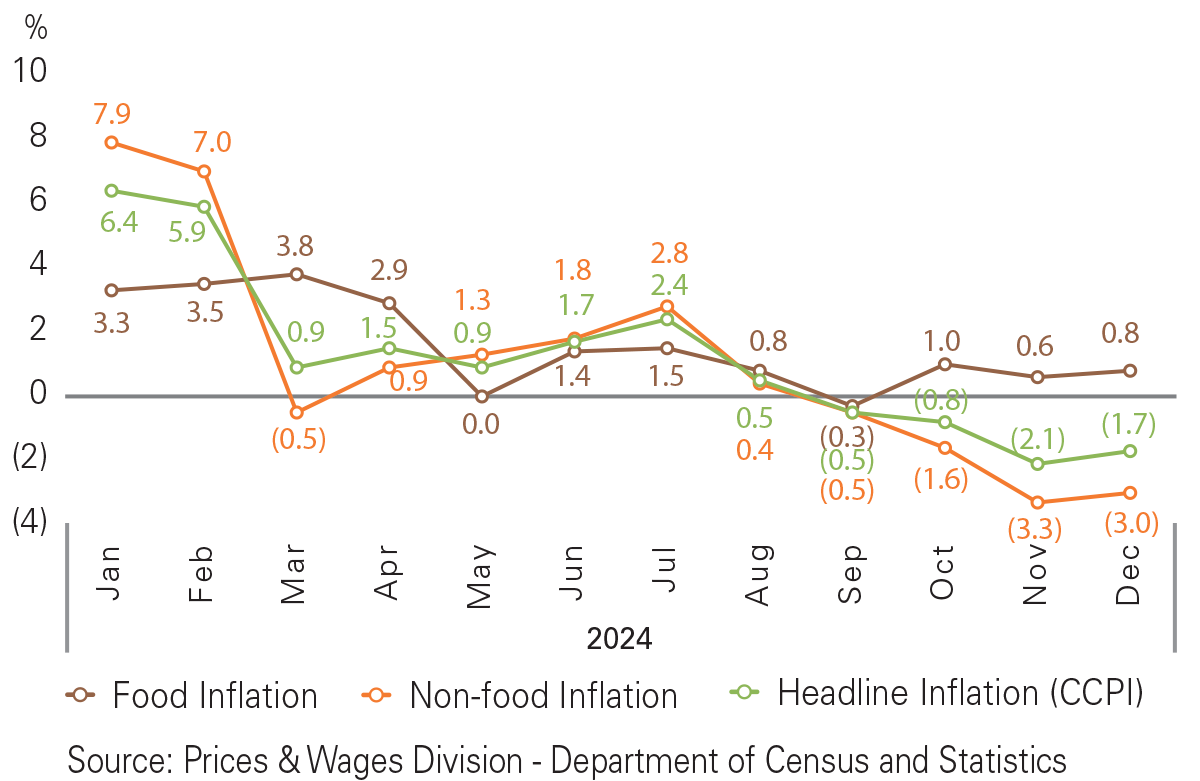

Inflation

Inflation maintained a downward trajectory, with headline inflation standing at -1.7% in December 2024.

Exchange Rate Movement

The Sri Lankan Rupee appreciated by 10% against the USD to Rs 292.58 during 2024 supported by enhanced inflows from workers’ remittances, tourist earnings and export conversions.

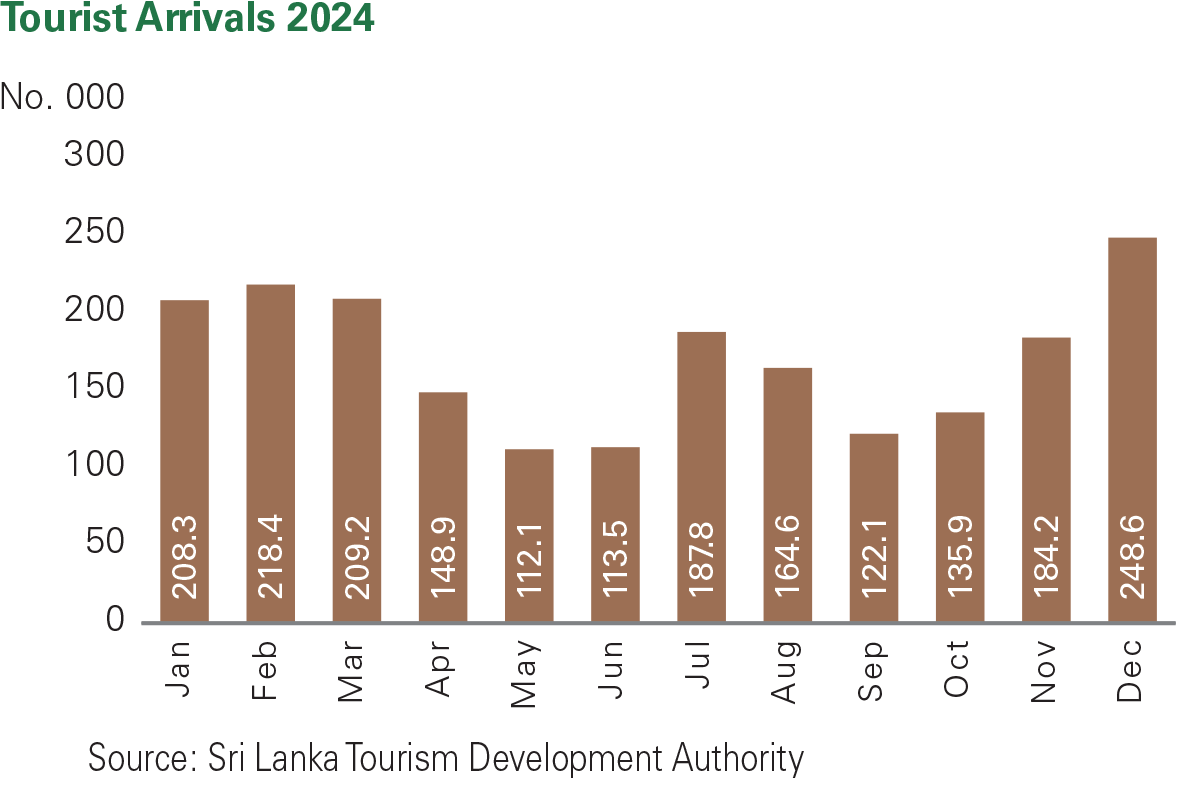

Tourism Sector Revival

The tourism sector continued to show signs of recovery with earnings expanding by 53.2% to USD 3.2 Bn as at end-December 2024.

Worker Remittances

Worker remittances maintained its upward trajectory expanding by 10.1% to USD 6.6 Bn as at end- December 2024.

Impact on Sampath Bank and Our Response

We proactively capitalised on opportunities that emerged from the gradual economic recovery, tailoring our strategy to facilitate business revival in economically significant sectors, including tourism, agriculture, renewable energy, healthcare and trade. Specific emphasis was placed on supporting and building resilience within the SME sector, through customised lending, expert advice and guidance to improve business operations and strategic planning through the expertise of the Business Revival Unit.

The Bank also focused on strengthening its market position in the remittance market. Furthermore, the Bank accepted the local bonds option in the GOSL’s ISB restructuring, converting 30% of the dues into Sri Lankan Rupee bonds and accepting new USD bonds for the remainder which was subject to a 10% haircut. Accordingly, impairment charges of Rs 15.8 Bn recognised for the ISBs were reversed. Overall, our strategic efforts contributed to a 59.4% increase in PAT and a ROE of 17.74% which stood among the best in the industry.

|

|

|---|---|

|

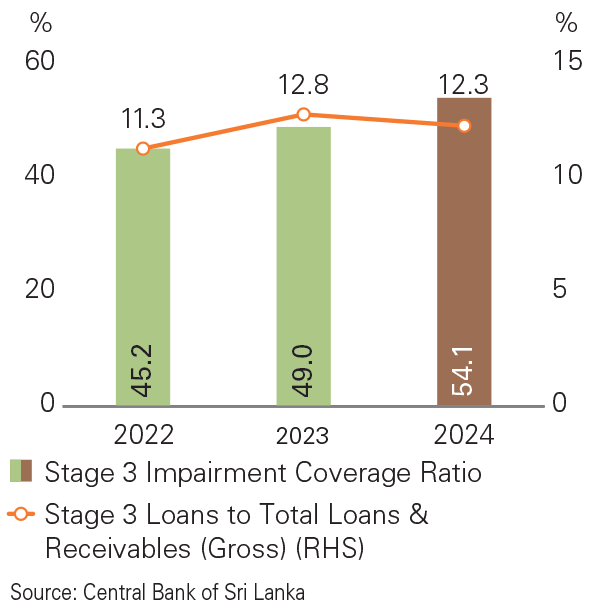

Impact on Sampath Bank and Our ResponseStriking a balance between responding to the needs of our customers and preserving asset quality, we engaged proactively with vulnerable customers offering revised payment plans to support business recovery. Financially distressed businesses with future potential were assigned to the Business Revival Unit for intensive monitoring and business restructure. The Bank also re-organised its SME lending unit to enhance support to small business. A range of digital solutions and financial literacy programmes conducted during the year continued to support financial inclusion in lesser served regions of the country. Moreover, the Bank maintained its commitment to its flagship CSR initiatives driving impactful change within the community. |

|

|

|---|---|

|

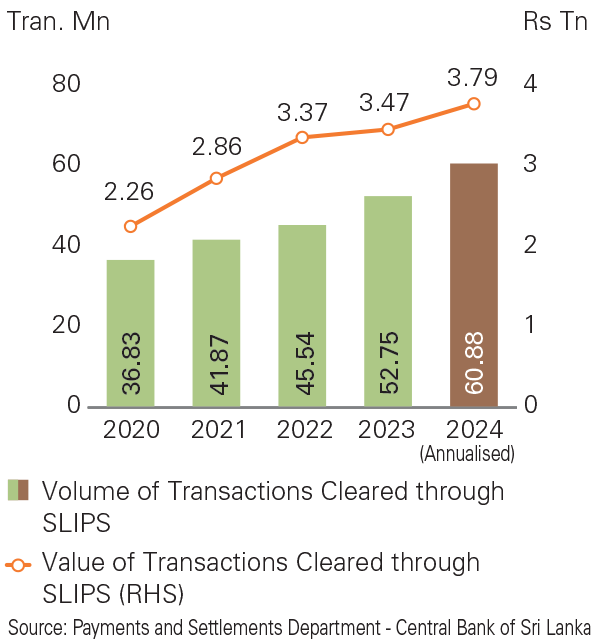

Impact on Sampath Bank and Our ResponseOur digital strategy strives to harness the full potential of technology while mitigating cybersecurity risks. We offer numerous digital solutions to customers including Sampath Vishwa, WePay and the mobile application. These solutions eliminate the need for branch visits, enhances accessibility and promotes ease of use through trilingual interfaces. The Bank also leverages technology to streamline processes and automate routine tasks to improve operational efficiency and accuracy. Data driven insights derived from advanced data analytics has strengthened decision-making while ongoing investments in the Bank’s cybersecurity architecture has safeguarded the Bank against cyber threats. |

|

|

|---|---|

|

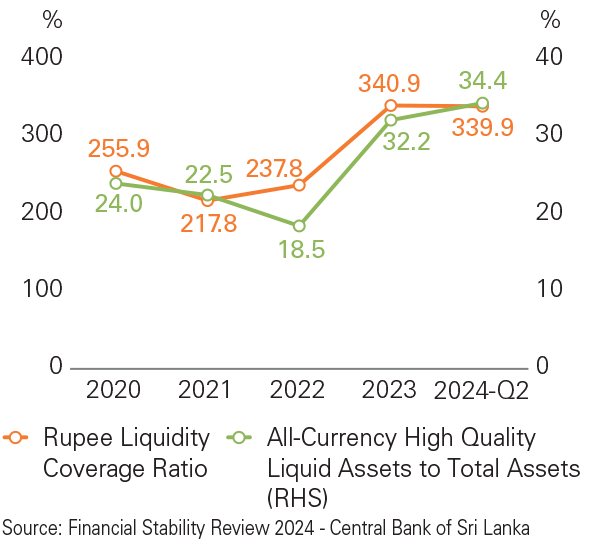

Impact on Sampath Bank and Our ResponseCognisant of its impact as a provider of finance, Sampath Bank continued to drive sustainable practices within and along its value chain. Financing the renewable energy sector is a key priority for the Bank while a range of initiatives including green loans, the sustainable green financing scheme, green leases and the ESMS system promotes and prioritises lending to sustainable business ventures. Ongoing efforts to minimise its own environmental footprint led to equipping 9% of branches with solar panels, conscious reductions in paper consumption and e-waste, and the promotion of digital platforms for banking. The Bank continued to invest in numerous flagship environment-related CSR initiatives, re-iterating its commitment to driving towards a more sustainable future. |

|

|

|---|---|

|

Impact on Sampath Bank and Our ResponseThe Bank proactively monitored the developments in the legal landscape and aligned its processes with the new requirements to ensure compliance with all laws and regulations in a timely manner. |